Crowdfunded Startups Die Slower Than VC-Backed Ones

We audited 4,338 companies that raised from retail investors between 2020 and 2022. Most aren't dead. They're just invisible.

Prelude: A Roll Call for the Missing

You are the slow money. The dumb money. The exit liquidity, the late chair, the gullible one.

You show up after the smart hands have cashed out, drawn by the word opportunity and the rumor of a future that was already priced in by the time you arrived.

You’re the retail investor the headlines wave away with a sigh. The bagholder in the meme rally. The $500 check on a Wefunder page. The name on a cap table nobody takes meetings with.

This is the story the industry keeps telling about you. It is repeated on cable, on X, on earnings calls, in the half-apologies of a SEC commissioner explaining why for your own protection some doors remain shut.

What we found wasn’t what we were told.

Movement I: Who Gets to Be Trusted With Capital

TLDR: For half a century, the SEC has gated private markets with a paternalist argument: regular people must be protected from themselves. Regulation Crowdfunding was the first major crack in that gate. Nine years in, nobody has graded the test.

There is a phrase in the accredited-investor rules that does a lot of quiet work. It says the restrictions exist to protect “unsophisticated” investors. The implication is clean and paternalistic: if you don’t have a million dollars in net worth or a six-figure salary, the agency will keep you away from private placements, because you cannot be trusted to know what you are buying.

Regulation Crowdfunding — legal since 2016, authorized under the JOBS Act — was the first serious test of that claim. It lets any American with a brokerage app invest up to a capped amount in U.S. private companies. No accredited gate. No placement memo. A Form C, a portal listing, a button that says Invest.

The skeptical story hardened almost immediately. Crowdfunded startups fail more than VC-backed ones. Retail investors get the last rounds, the zombie rounds, the companies that couldn’t attract a real check. These claims saturate finance Twitter and op-ed pages. They have the texture of expertise. They are almost entirely unaudited.

So we audited them.

Movement II: What the Numbers Actually Say

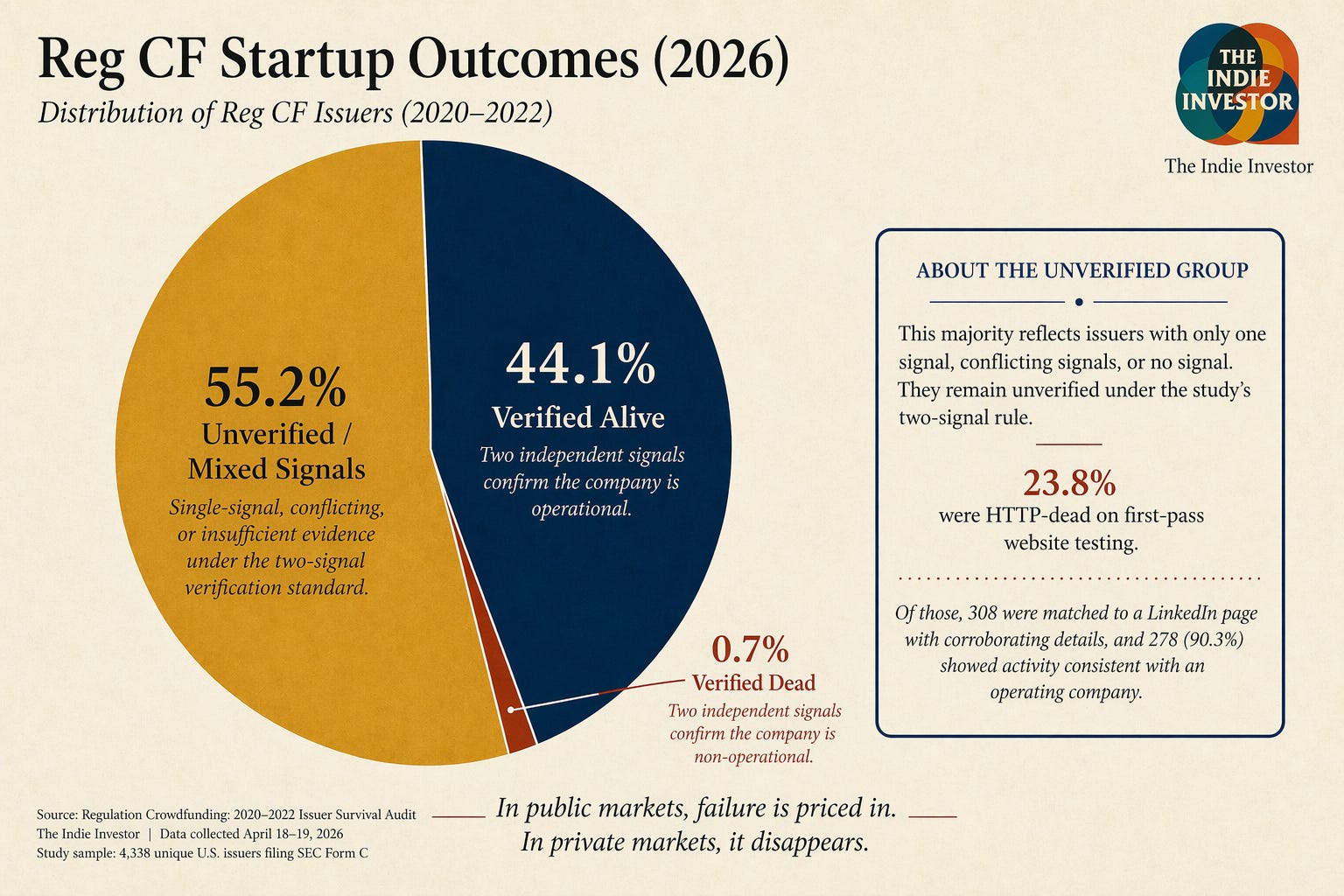

TLDR: 44.1% of the cohort is verifiably alive. 0.7% is verifiably dead. The rest sit in a gray zone of unverifiable existence — not because they failed, but because nobody has been paid to check.

We pulled every initial Form C filing from SEC EDGAR between January 2020 and December 2022 — 4,338 unique companies. We tested each filed website for HTTP liveness, then independently matched each issuer to a LinkedIn company page via Google and ran a two-factor cross-check: does LinkedIn’s listed website match the SEC filing? Does the name match? Both matches meant CONFIRMED. Neither meant we’d caught one of Google’s casual errors — and we caught 455 of them, 10.5% of the sample.

The final tally is not subtle.

1,913 of 4,338 (44.1%) verified alive. Live site, corroborating LinkedIn presence, at least one active signal.

30 of 4,338 (0.7%) verified dead. Thirty. Three-zero.

2,395 (55.2%) unverified. Evidence on one axis, silence on the other.

The gray zone is not a story about failure. It is a story about attention. No regulator writes obituaries for small crowdfunded companies. No Twitter account tracks them. When a Reg CF issuer goes quiet, the quiet is not proof of death — it’s proof no one is watching.

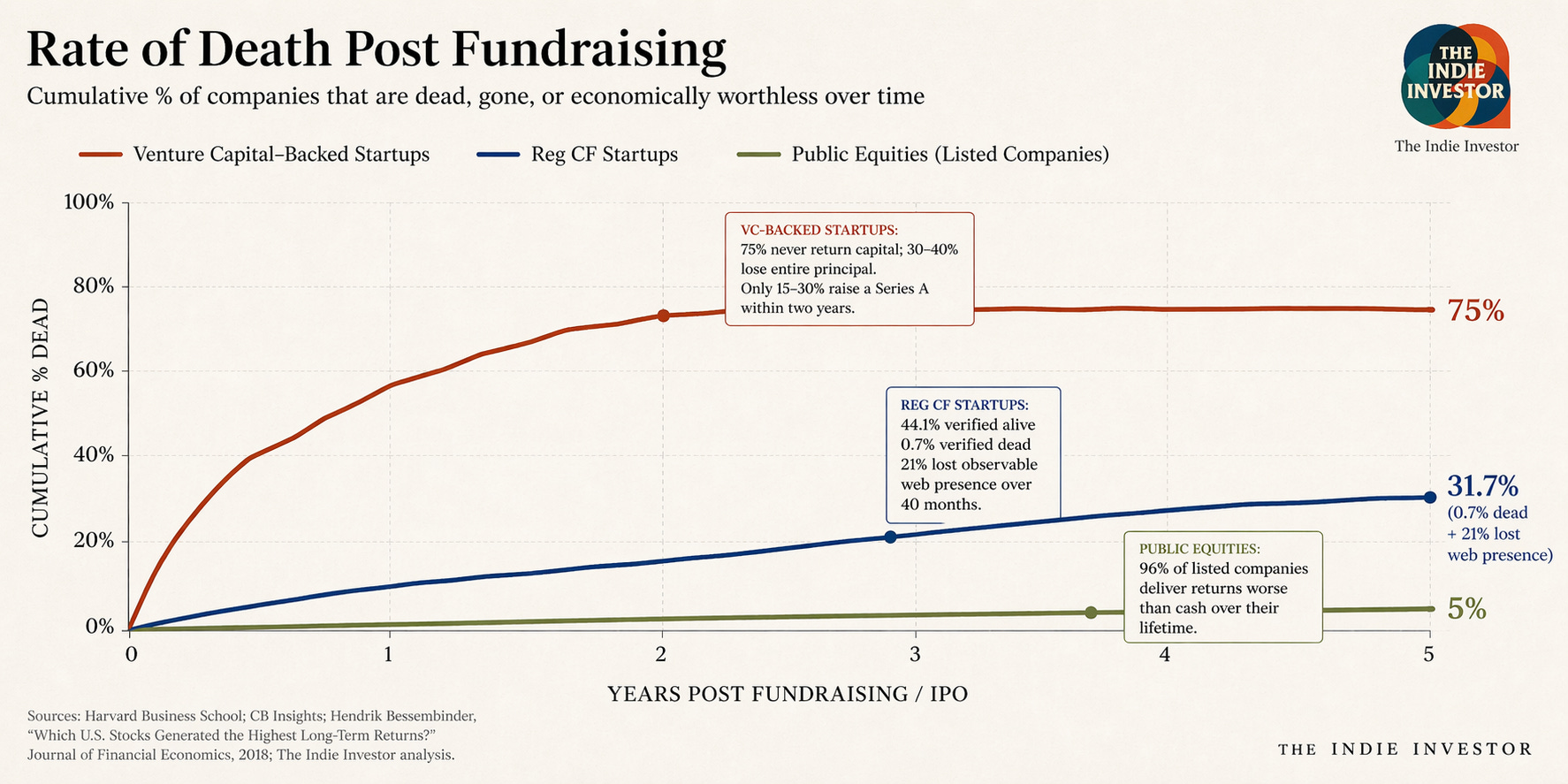

The Wayback Machine confirms the shape. Between end of 2022 and April 2026, cumulative web presence across the cohort fell from 95.3% to 79.1% — a 704-company decline over 40 months. Every cohort shows the same pattern: a year of grace post-raise, a wave of attrition, a long slow fade. The graveyard is real. It fills like graveyards have always filled — not with catastrophe, but with quietness.

And many of the apparent deaths are illusions. 1World Online, a Wefunder issuer whose filed URL no longer resolves, has 4,074 followers on LinkedIn and 42 employees. EX Venture, a Republic issuer in similar shape, has 3,886 followers and 39 staff. Kitsbow Apparel PBC, a public benefit corporation funded on Wefunder, has 1,504 followers and nine employees. An investor who reads only the website misses half the picture. An investor who reads only LinkedIn misses the other half.

Movement III: The Comparison That Breaks the Argument

TLDR: If retail crowdfunding’s failure rate is grounds to gate regular people out of private markets, then venture capital and the public stock market should be gated by the same logic. Neither has numbers this good.

Between 2020 and 2022, Americans put roughly $1.2 billion into Reg CF companies — about $239 million in 2020, near $500 million in 2021 (the sector’s record year), another $500 million or so in 2022 (Crowdfund Capital Advisors; KingsCrowd).

Over the same three years, U.S. venture capital deployed approximately $747 billion (PitchBook–NVCA Venture Monitor): $164B, $344.7B, $238.3B. Reg CF is 0.16% of the total. The entire three-year retail-equity haul clears in about thirty-two hours of 2021-pace Silicon Valley deal flow.

The “risky” class of capital is six hundred times smaller than the “serious” one. That is the scale.

Now the survival.

Venture capital: 75% of VC-backed startups never return capital; in 30–40% of investments the entire principal is lost (Harvard Business School; CB Insights). Only 15–30% of seed-stage companies raise a Series A within two years. The capital class above Reg CF is not operating a safer product.

Public equities: Hendrik Bessembinder’s 2018 Journal of Financial Economics study of every listed U.S. stock since 1926 found that the median stock over its lifetime returns less than one-month Treasury bills. Only 4% of listed companies account for the entire net wealth gain of the U.S. stock market since 1926. The other 96% collectively matched cash.

Reg CF: 44.1% verified alive, 0.7% verified dead, 21% lost observable web presence over 40 months.

This is where the folk narrative breaks. The argument regular people shouldn’t be allowed into this has always rested on the implied comparison that regular people have better, safer options elsewhere. They don’t. Every venue in American capital has the same basic mathematics — most names lose, a few win spectacularly, the difference is which names and by how much. The gate was never really about risk. It was about who gets to sit at the table before the winners sort themselves from the losers.

Reg CF lets a thousand people with a hundred dollars each sit at that table. Nothing else in American finance does.

Finale: An Invocation for the Indie Investor

When the dominant narrative about an asset class is built on folk wisdom rather than data, the indie investor’s job is to do the counting herself — before the money moves, and after.

Read the Form C, then the LinkedIn page. A filed website that 404s is not an obituary. A quiet storefront with 4,000 LinkedIn followers is a company hiring through back channels. The two-signal rule isn’t just methodology — it’s the minimum standard for honest due diligence on any private investment.

Audit before the check clears. Before you click invest, check the issuer’s site, their LinkedIn, their most recent Form C-U progress update, a Wayback snapshot if the domain looks thin. If two of four are missing, ask why.

Let the portal’s track record inform the bet. StartEngine issuers are 3.5× more likely to be traceably alive four years post-raise than MainVest issuers. Some of that gap is measurement artifact — LinkedIn is sparse for restaurants and breweries — but the rest is business quality, and the retail investor deserves to know the difference before she chooses.

Reject the paternalism. When someone tells you private markets are too risky for you, ask them for the failure-rate math on the public markets. Then ask for the failure-rate math on venture. Then watch the subject change.

Keep watching. The gray zone — 55% of the cohort — is a story about who gets paid to document small companies. The answer is: nobody. That work falls to the Indie Investor, or it doesn’t get done.

Capital wants to circulate while belief wants to compound. The audit is how we make sure neither one is being stolen while the rest of us are told to look away.