Who Profits When Policy Gets Reversed

On tariff refund rights, private equity, and the secondary markets built around government uncertainty

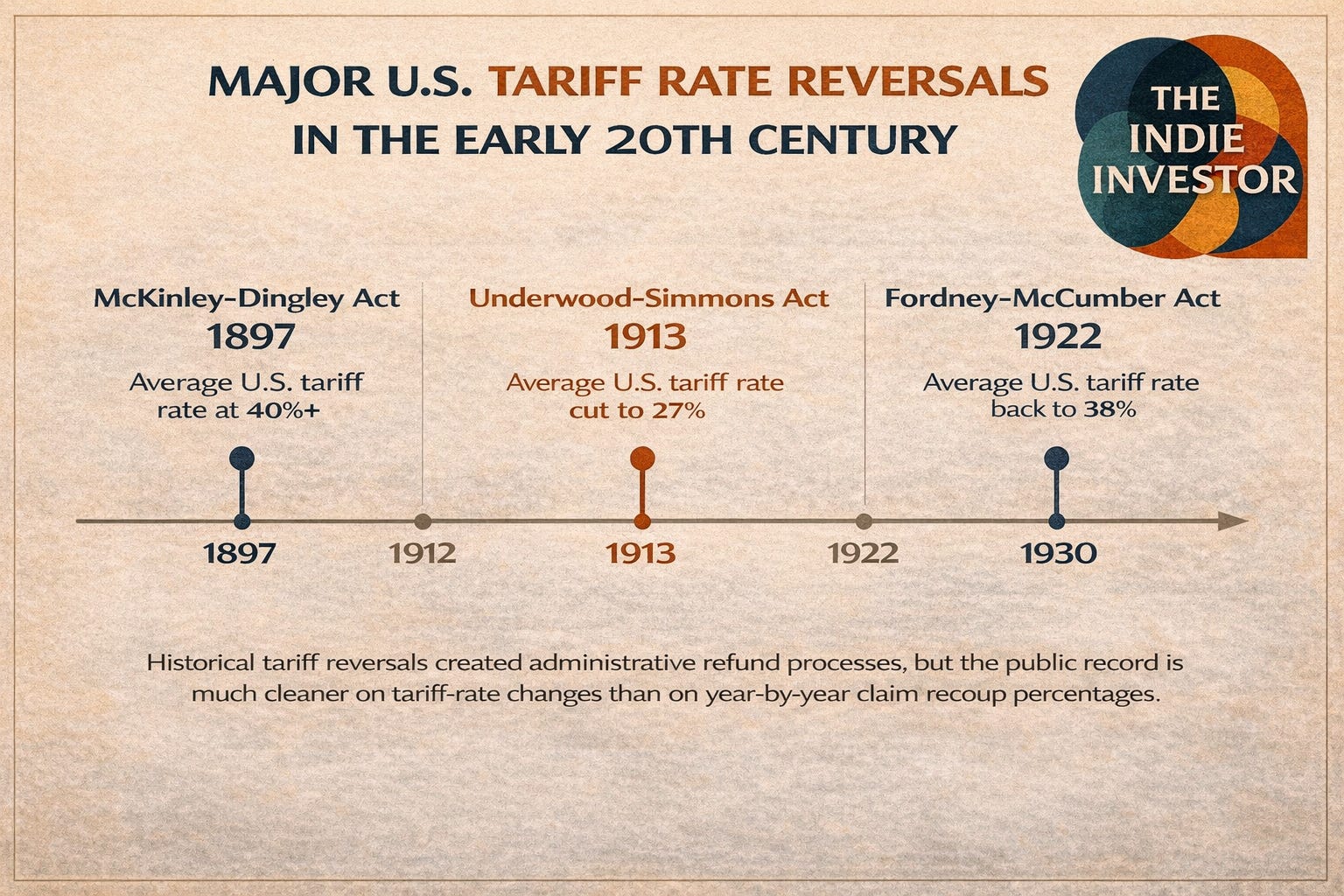

Prologue: The Refund That Hasn’t Happened Yet

The money was already paid.

Stamped. Cleared. Forgotten.

A line item at the border.

A cost absorbed into price.

Passed along, diluted, disappeared.

Years later, a ruling.

A sentence that bends time backward.

Maybe it shouldn’t have been collected.

Maybe it comes back.

But not as it left.

Now it returns as a question.

A claim.

A process.

Filed. Contested. Deferred.

The refund exists first on paper.

Then in probability.

Only sometimes in cash.

And somewhere in between,

it changes hands.

Discounted. Aggregated.

Waited on by someone else.

By the time it arrives,

if it arrives,

it already belongs

to someone who knew how to wait.

Movement I: What Are Tariff Refund Rights, Actually?

TLDR: When tariffs are overturned, refunds don’t flow back but instead turn into tradable claims. And those claims are often bought by institutions before consumers ever see the cash.

Policy moved first. Markets followed later.

A recent Supreme Court decision called into question the legal foundation of certain tariffs imposed under executive authority. At the center is a narrow but consequential issue: whether those tariffs were lawfully applied in the first place. If they were not, the implication is simple in theory and complex in practice as duties may have been collected without proper authority.

But the real question is not legality, as the Supreme Court has weighed in and guided that the President lacked the powers to enact sweeping tariffs, but now the issue is timing.

Are those tariffs considered unlawful from inception, meaning importers are owed refunds for past payments?

Or are they only invalid moving forward, leaving prior collections untouched?

The answer determines whether billions of dollars exist as a potential asset or disappear as history.

If refunds are permitted, they do not arrive automatically. Importers who paid duties must file claims through administrative channels, often navigating years of process across agencies, courts, and appeals. Documentation must be produced. Eligibility must be proven. Outcomes remain uncertain.

Time stretches. Probability fragments.

This is where finance enters.

A refund that is delayed, disputed, or uncertain is no longer just a legal matter. It becomes a contingent asset. And contingent assets can be priced.

Importers holding potential claims face a choice: wait years for an uncertain payout, or sell the right today at a discount. That discount reflects time, risk, and complexity. For the right buyer, it reflects opportunity.

Private equity firms, litigation finance funds, and specialized claim investors step into this gap. They underwrite the probability of success, the duration of the process, and the expected recovery. They purchase claims at a fraction of face value and assume the burden of waiting, litigating, and collecting.

This is not new. It mirrors how markets formed around distressed assets in other domains; bankruptcy claims in the wake of corporate collapses, including FTX, where retail creditors sold future recovery rights to institutional buyers at steep discounts. What appears to be chaos at the surface becomes structured opportunity underneath.

The pattern is consistent.

When outcomes are delayed, capital accelerates them.

When payouts are uncertain, markets price them.

When uncertainty meets bureaucracy, capital forms a market.

Movement II: How Private Equity Prices Policy Reversal

TLDR: Institutions don’t speculate on policy reversals but instead underwrite them, pricing risk, time, and probability. By the time the public hears about refunds, the claims have already been bought and structured.

If you walked onto a securitization desk the week after a ruling like this, no one would be debating fairness. No one would be asking whether refunds should reach end customers. The conversation would be quieter, more mechanical.

How big is the pool?

How clean are the claims?

How long until cash actually moves?

This isn’t speculation.

It’s underwriting.

You start with size. The headlines are irrelevant to the exposure. What’s the total universe of tariffs that could plausibly be refunded? How much of that is actually claimable? Then you haircut it. Not every importer files. Not every claim survives scrutiny. Not every dollar makes it through appeals.

Next is probability. Legal teams don’t ask “will we win?” They ask “what’s the weighted path?” District courts, appellate courts, administrative review. Each step gets a percentage. Multiply it out. That’s your expected recovery.

Then time. Time is everything. A refund paid in five years is not the same asset as a refund paid in twelve months. You discount accordingly. Aggressively. Bureaucracy has a cost of capital.

And layered on top of that is policy risk. Could this be narrowed on appeal? Delayed through process? Quietly neutralized by Congress? Enforcement risk sits there too with winning a claim being one thing, collecting on it is another.

By the time you’re done, you don’t have a legal opinion.

You have a price.

Legal probability.

Timing discount.

Liquidity risk.

That’s the model.

So when these funds approach importers, the pitch is simple: take certainty now, or wait in uncertainty. Cash today at 10 to 30 cents on the dollar, versus a full payout that may or may not materialize years from now. For businesses managing cash flow, that’s not an abstract choice but a well-received lifeline that could determine survival.

From the outside, it looks like opportunism. From the inside, it looks like structure. Claims get aggregated. Risk gets pooled. Downside gets hedged across portfolios of outcomes. What began as a policy reversal becomes something closer to a financial product.

And this is the part most people miss.

Retail reads headlines about refunds.

Institutions quietly buy the right to the headline.

By the time the public debates eligibility, the claims are already securitized.

Movement III: The Broader Pattern Of Monetizing Volatility

TLDR: Tariff refund rights feel novel only because they’re visible. The mechanism itself is not.

This is part of a broader pattern that has quietly expanded across markets over the last decade. When outcomes become uncertain—legally, administratively, or politically—capital doesn’t retreat. It reorganizes.

You saw it with FTX, where bankruptcy claims began trading almost immediately after collapse, long before final recovery values were known. Creditors, many of them retail, sold their claims at steep discounts. Institutional buyers stepped in, aggregating positions and underwriting the eventual payout.

You saw it again with Silicon Valley Bank, where receivership claims and asset recovery paths became investable exposures. During COVID, relief programs designed as emergency support created secondary markets of their own; claims, credits, and entitlements priced and traded before many recipients fully understood their value.

The same logic applies across tax credit markets, from renewables to film financing, where future benefits are sold forward for present liquidity. It appears in litigation finance, where lawsuits become portfolios. In eminent domain cases, where land seizures turn into structured payouts. In structured settlements, where individuals trade long-term payments for discounted cash today.

Different assets. Same pattern.

We are living in an era where legal uncertainty becomes yield.

Administrative delay becomes arbitrage.

Policy reversal becomes a tradable event.

The connective tissue is time and complexity. The longer it takes for an outcome to resolve, and the harder it is to navigate the process, the more likely it is that a secondary market will form. One side sells certainty. The other side buys optionality.

And this is where the divide sharpens.

Retail participants experience volatility as disruption, as something to avoid, something to wait out. Institutions experience that same volatility as raw material. Something to structure, price, and distribute.

The volatility that scares retail is the volatility institutions securitize.

Once you see the pattern, it’s difficult to unsee. Markets are no longer just reacting to events. They are forming around the resolution of those events, long before the final outcome is known.

Finale: The Indie Investor Guide

Policy shifts create headlines. Markets form in the delay between the headline and the outcome.

The instinct is to focus on the event itself and not the ruling, the reversal, the potential payout. But in practice, value rarely sits at the surface. It moves through process, timing, and structure. For anyone navigating these moments, the edge is not in predicting outcomes. It’s in understanding how those outcomes are intermediated.

Understand the plumbing before the headline.

Legal reversals do not automatically translate into cash flows. They initiate processes such as claims, filings, reviews, appeals. Each layer introduces friction, delay, and variability. The path from entitlement to payout is where most of the value is reshaped.

Follow who is buying the claim.

When institutional capital enters early, it does so with a model. Assumptions are being made about probability, timing, and recovery. Observing where that capital concentrates—and under what terms—often reveals more than the headline itself.

Price time, not just outcome.

A nominal payout is only one dimension. Duration changes everything. A full recovery years from now carries a different value than partial liquidity today. Time is not a backdrop but becomes its own distinct asset class.

Beware of asymmetry.

By the time broader awareness builds, many of the highest-optional positions have already been acquired, structured, or stripped of upside. Late participation often means engaging with a reshaped version of the opportunity.

Broaden your lens.

The opportunity is rarely the refund itself. It is the ecosystem that forms around it including claims trading, financing structures, aggregation, and distribution. The primary event creates motion. The secondary market captures it.

Policy does not simply redirect capital.

It reorganizes it.

Government policy doesn’t just move markets.

It creates new ones.