Who Owns Your Data When Storage Gets Expensive?

On rising memory costs, AI demand, and the quiet shift from distributed computing to institutional control

Prelude: The Curve That Learned to Bend

It began as a line.

A quiet slope.

Predictable.

Measured in increments no one questioned.

More supply,

less cost.

More storage,

less thought.

The rhythm held.

Until it didn’t.

A second line entered.

Not parallel.

Not patient.

It pressed.

Closer.

Faster.

Steeper-

than the system was built to absorb.

You could feel it before you could name it.

Latency where there was none.

Cost where there was silence.

Friction in places that once felt infinite.

The lines began to speak to each other.

One pulling upward.

One refusing to move.

A tension.

Not visible.

But audible.

Like a bow drawn too tight

across a string that was never meant

to carry this much weight.

Again.

Pressure.

Allocation.

Reallocation.

Again.

Capacity.

Constraint.

Constraint.

Again.

Something is being asked of the system

that it cannot evenly give.

And so it chooses.

Not everything rises.

Some things are left behind.

Some demands are no longer met.

Not because they disappeared—

but because something else

learned how to ask louder.

Faster now.

The curve is no longer a curve.

It bends.

It sharpens.

It begins to fold into itself.

And somewhere in that fold,

something that once felt distributed

starts to converge.

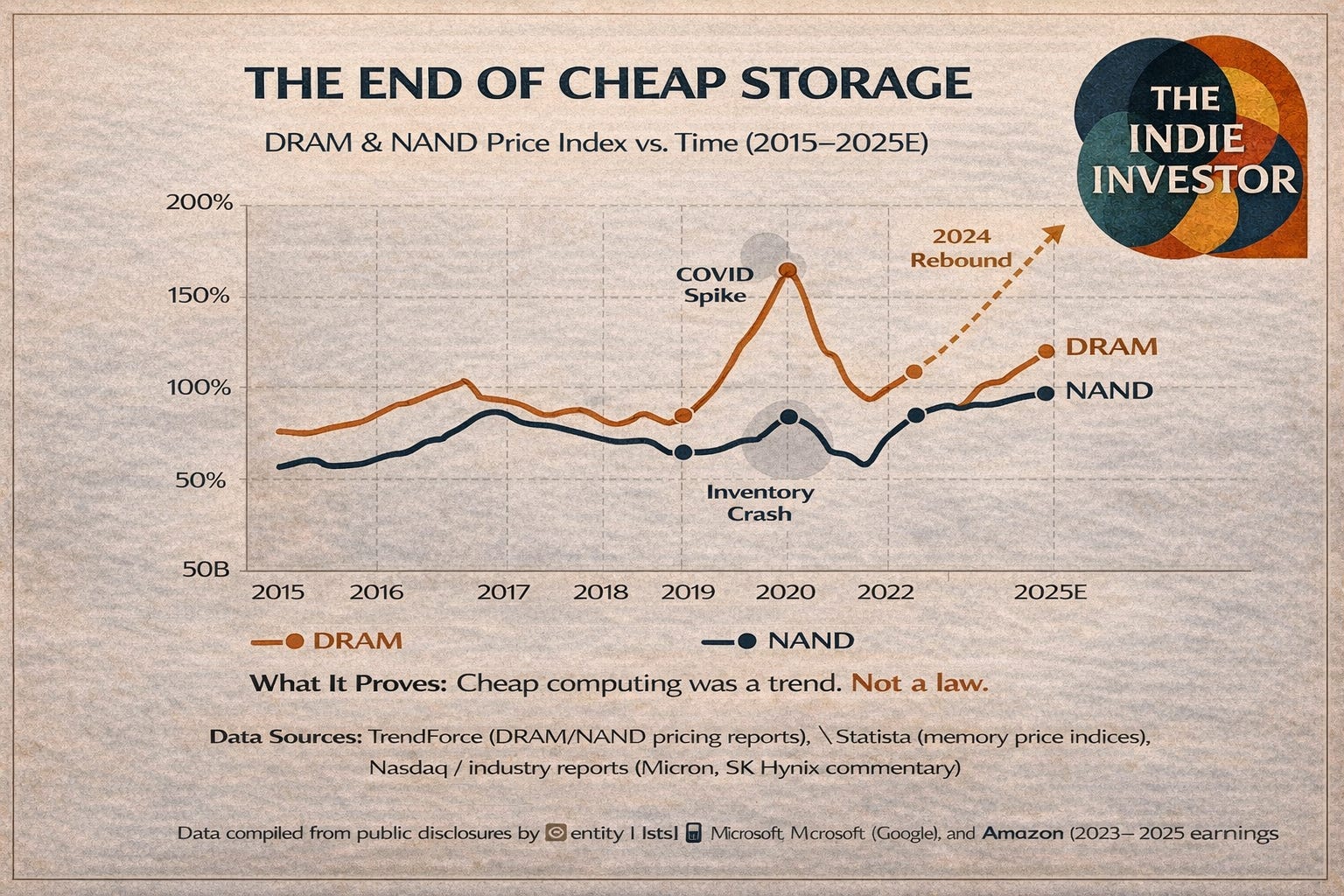

Movement I: When Storage Stopped Getting Cheaper

TLDR: Cheap computing was a supply chain condition, not a guarantee. As memory markets tighten and costs rise, abundance is giving way to tradeoffs.

For most of the last three decades, computing followed a quiet promise. Next year would be cheaper.

Memory costs declined with near-clockwork regularity. DRAM prices fell over long arcs. NAND storage expanded while becoming more affordable. The cost of adding capacity, whether in a laptop or a data center, felt marginal. This was not just a technical trend. It became cultural. Consumers came to expect more storage, more speed, and lower prices with each upgrade cycle. Businesses built budgets around it. Entire workflows assumed it.

That assumption has broken.

The inflection did not come from a single event. It came from a collision of forces. COVID-era demand spikes pulled forward years of device purchases and strained semiconductor supply chains that were optimized for efficiency rather than resilience. At the same time, production disruptions from fab shutdowns and logistics bottlenecks tightened availability. By 2022, the industry swung in the opposite direction. Excess inventory met slowing demand, pushing memory prices downward in the short term. The correction did not restore balance. It exposed how fragile the system had become.

By 2023 and into 2024, the structure of the market had shifted.

The global memory industry is now highly concentrated. Samsung, SK Hynix, and Micron control the majority of DRAM supply. In downturns, they reduce production to stabilize pricing. In upcycles, they allocate capacity toward higher-margin segments. This is not a perfectly elastic market. It is managed.

Recent data reflects the shift. After bottoming in late 2022, DRAM prices began rising again through 2024, with some segments increasing significantly depending on configuration and contract structure. NAND flash followed a similar, though more volatile, pattern. Pricing swings are now driven as much by supply discipline as by end demand. At the device level, memory and storage account for a meaningful share of total cost, often between 15 and 25 percent for consumer PCs and higher for performance systems.

For consumers, the change appears gradually. Entry-level devices stagnate. Mid-tier upgrades feel less compelling. Configurations that once felt standard, such as 16GB of RAM or 512GB of storage, begin to carry noticeable premiums. The expectation of abundance gives way to tradeoffs.

For businesses, the signal is clearer. Storage is no longer a background cost. It is a line item with volatility.

Cheap computing was never guaranteed. It was the result of a supply chain that, for a period, delivered more than the market demanded. That balance has shifted. When the cost curve flattens or reverses, the systems built on top of it begin to adjust.

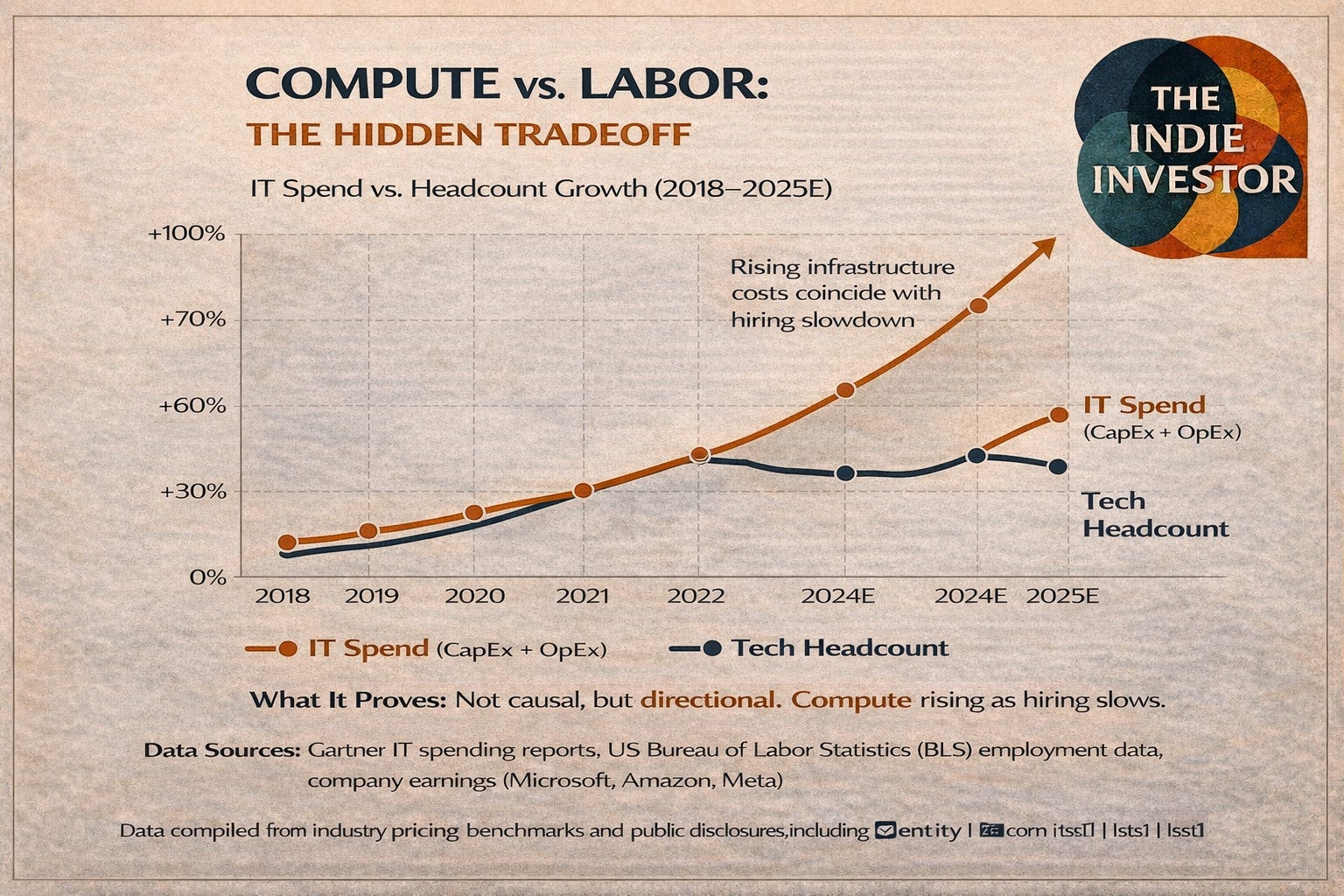

Movement II: The Employment Signal Hidden in Hardware

TLDR: When compute gets more expensive, it doesn’t stay in IT budgets. It reshapes hiring, forcing companies to balance infrastructure costs against labor.

Hardware rarely shows up in conversations about hiring. It sits in a different column, owned by a different team, approved through a different process. But when the cost of compute shifts, it does not stay contained. It moves.

For most of the last decade, companies expanded under an assumption that felt invisible at the time. Devices were cheap enough to provision widely. Storage scaled without forcing tradeoffs. Compute was abundant enough that adding a headcount did not require rethinking infrastructure. A new hire meant a laptop, access to systems, and marginal incremental cost.

That math is tightening.

The divergence highlights a shift in resource allocation: capital increasingly flows toward compute capacity rather than labor expansion.

As memory and storage costs rise, IT budgets are no longer a quiet backdrop. They become a constraint. Every dollar allocated to infrastructure is a dollar that competes with something else. In many cases, that something else is labor.

You can see it in subtle shifts first. Device refresh cycles stretch from three years to four, sometimes longer. Standard configurations are reconsidered. Not every employee receives the same level of provisioning. Storage quotas appear where none existed before. These are small adjustments, but they accumulate.

At the enterprise level, the tradeoffs become more explicit. Capital expenditure on hardware and infrastructure begins to rise at the same time companies are under pressure to control operating expenses. Finance teams start asking different questions. Does this team need dedicated resources, or can workloads be centralized? Can compute be shared rather than distributed? Can fewer people do more with constrained systems?

The conversation changes shape. It becomes less about growth and more about efficiency.

Data from recent enterprise surveys reflects this shift. IT spending as a share of overall budgets has increased in certain sectors post 2022, while headcount growth has slowed or reversed in parallel. Device replacement cycles have lengthened across both consumer and enterprise environments. These are not isolated trends. They are signals of reprioritization.

When compute was abundant, it faded into the background and allowed labor to scale without friction. When compute becomes constrained, it moves to the foreground and forces choices.

The relationship is not always direct. Companies do not reduce hiring simply because RAM is more expensive. But they do operate within budgets. And when infrastructure costs rise, those budgets absorb the impact somewhere.

For years, the narrative around work focused on talent, culture, and productivity. Less attention was paid to the physical and digital systems that make that work possible. That gap is closing.

When the cost of compute changes, the shape of the workforce changes with it.

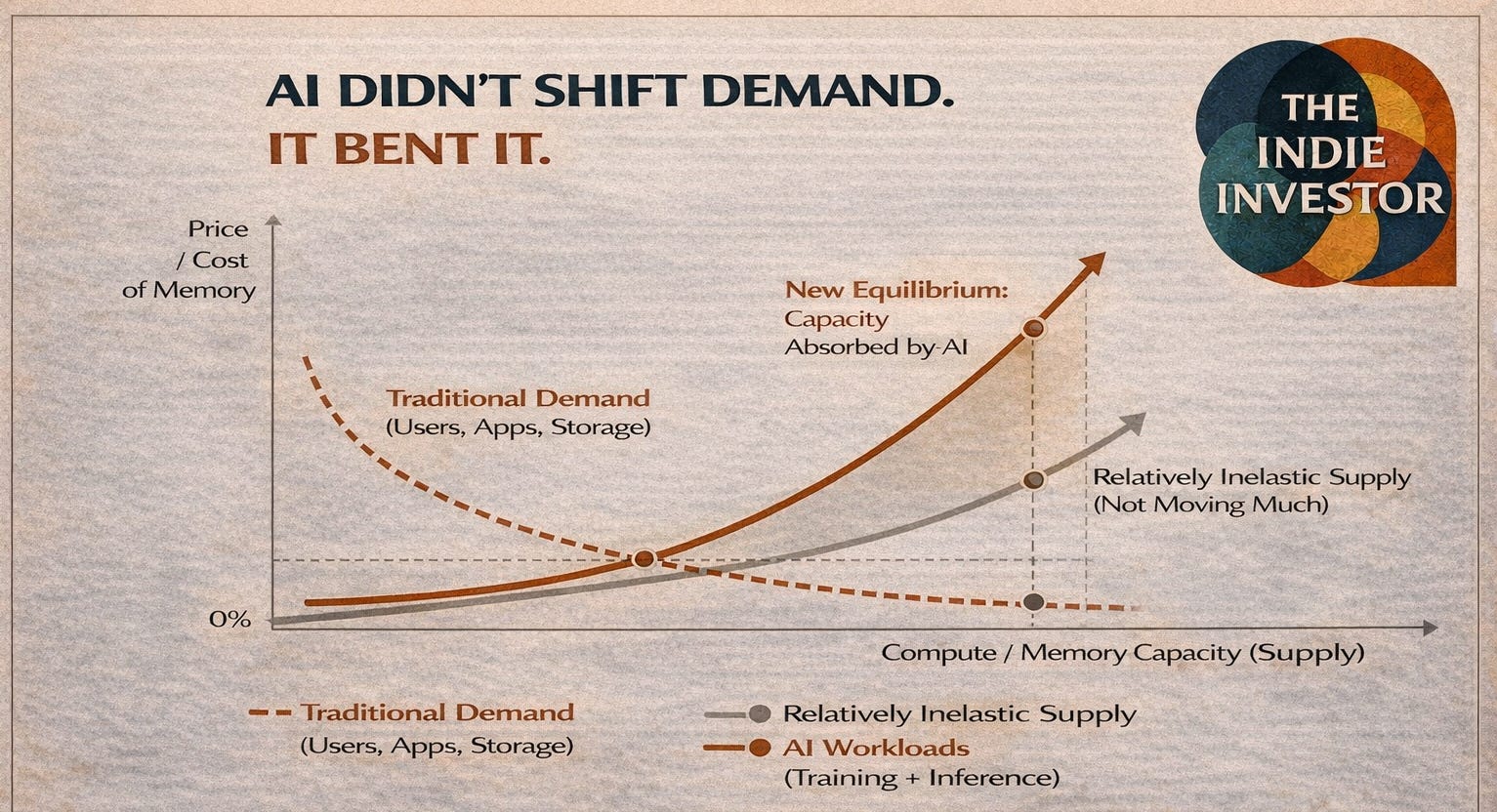

Movement III: AI Broke the Demand Curve

TLDR: AI has shifted demand for storage from human use to machine training, pulling supply upward and leaving the rest of the market to absorb the constraints.

For years, demand for storage followed a familiar rhythm. More users, more files, more applications. Growth was steady, predictable, and tied to human activity.

AI changed the shape of that demand.

This is not just an increase. It is a reclassification of what storage and memory are for. Data is no longer simply stored. It is ingested, processed, retrained, and redeployed at scale. The system is no longer passive. It is constantly in motion.

That shift carries a different set of requirements. AI workloads depend on high-bandwidth memory, tightly coupled with GPUs, and vast storage pipelines that can move and access data without delay. Latency matters. Throughput matters. Capacity alone is not enough.

Supply has not kept pace.

A growing share of advanced memory production is now directed toward AI infrastructure. Hyperscalers and large enterprises are absorbing capacity at a rate that reshapes allocation across the market. What used to flow toward consumer devices and general enterprise use is increasingly diverted to training clusters and inference systems.

The result is pressure everywhere else.

Enterprises that are not operating at hyperscale are forced to compete for what remains. Smaller players move down the stack, sourcing less advanced components or accepting performance tradeoffs. Procurement cycles lengthen. Pricing becomes less predictable. What was once standardized begins to fragment.

Data reflects the shift. Capital expenditure from major cloud providers has accelerated sharply, with tens of billions allocated toward AI infrastructure in the last two years. High-bandwidth memory demand has grown at a pace that exceeds traditional supply expansion. Manufacturers prioritize these segments because the margins justify it.

This is rational behavior. It is also redistributive.

Storage is no longer primarily serving the storage of individual or enterprise data. It is serving the training and operation of intelligence systems that sit above those users. The hierarchy has inverted. Instead of infrastructure supporting people, infrastructure increasingly supports models that mediate how people interact with systems.

This is the demand curve breaking.

When a new class of workload arrives that is both capital intensive and margin accretive, it does not coexist quietly with existing demand. It displaces it.

The implications are not immediate, but they are directional. As more capacity is pulled into AI-driven use cases, the rest of the market adjusts around the edges. Costs rise. Availability tightens. Tradeoffs become visible.

Storage did not become scarce by accident.

It became scarce because something else became more valuable.

The Indie Investor Field Guide: A Field Guide to the Storage Wars

The cost of compute is no longer fading into the background. It is reappearing as a constraint. Not suddenly, not dramatically, but enough to change how decisions get made across individuals, companies, and institutions.

This shift does not require prediction. It requires awareness of where pressure is building.

1. Expect volatility, not decline

The long arc of falling storage and memory costs is no longer reliable. Prices may still move in cycles, but the structural floor is rising. Planning around perpetual cost reduction is no longer a safe assumption.

2. Separate price from capability

Lower-cost devices will still exist, but often through tradeoffs. Repurposed chipsets, constrained memory configurations, and reliance on external storage will shape what “affordable” computing looks like. The device may be cheaper. The system around it may not be.

3. Watch where compute is concentrated

Decisions about on-device, on-prem, or cloud-based computing are becoming economic choices as much as technical ones. As costs rise, more workloads will be centralized. Understanding where compute is moving helps explain where control is shifting.

4. Follow the supply chain, not the product

End-user devices are the output of a deeper system. Memory manufacturers, GPU producers, and infrastructure providers are setting the terms. Observing their constraints and priorities reveals more than any single product launch.

5. Recognize the shift in ownership

Local storage once implied control. As more data and processing move off-device, that relationship changes. Access replaces ownership. Convenience replaces independence. The tradeoff is subtle, but it compounds over time.

Computing has not disappeared.

It has become more expensive to distribute.

And when something becomes harder to distribute, it tends to concentrate.