Warnings, Everywhere, All at Once: Michael Burry vs. the Market’s Many Realities

Michael Burry in 2025, Manufactured Optimism, and the Mixed Signals of the Market

Prelude: Against the Chorus

A whisper moving across charts,

a shared flicker we pretend not to see.

But look closer.

It isn’t one prophet carrying fire;

it’s all of us tracing heat the way Prometheus once traced flames

before the world admitted it smelled smoke.

Each cycle finds new voices

founders, CEOs, investors alike

all noting the same brittle shimmer at the peak,

the subtle crack before the break.

And now, with AI burning white-hot,

valuations molten and optimism bright enough to blind,

the market gathers closer around the bonfire,

each of us trying to decide what we’re willing to lose to the flame.

The question isn’t whether the sky is falling,

but why we keep inching toward the heat.

For speak a warning once and it becomes myth;

speak it every cycle and it is a fable,

and still,

some sparks are worth watching.

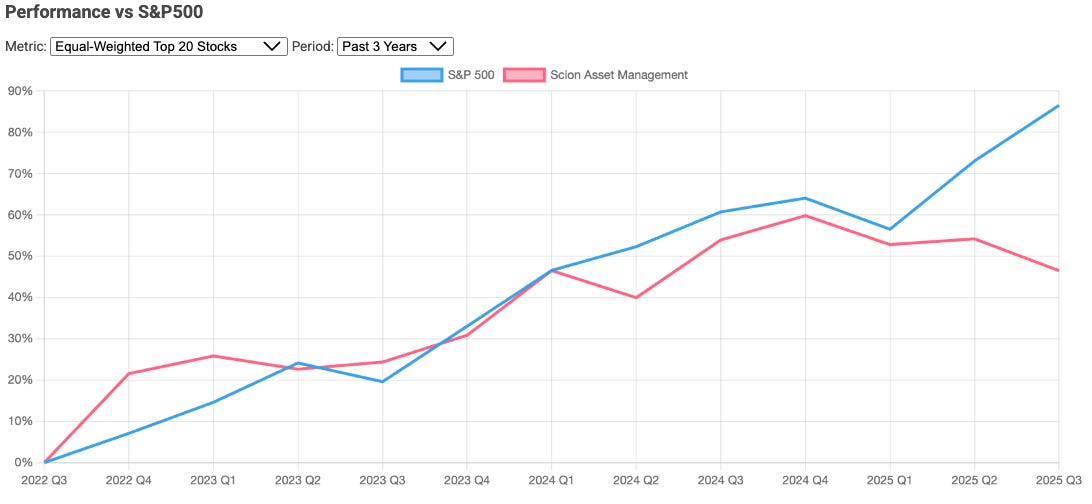

Movement I: Burry’s Shadow (And Market’s Doubt)

TLDR: His shorts were less about catastrophe and more about accounting, capital cycles, and narrative overextension.

Michael Burry’s name has become shorthand for the first canary in every coal mine.

Whenever valuations stretch, whenever optimism becomes feverish, whenever indices run faster than earnings, his silhouette reappears in headlines: “Burry Bets Big Against the Market.” It’s the easiest narrative the media has because every bubble needs a prophet, and every prophet needs a past.

But the reality of 2008 was far more painful and uncertain than the myth suggests.

During the subprime trade, his own investors threatened to sue him, believing he had gone rogue. Regulators investigated him because they couldn’t conceive of someone betting against the entire mortgage market without ulterior motives. And in the middle of it all, Burry — a medical doctor by training — faced the loneliness of being both right and doubted at the same time.

“He’s clearly a contrarian investor, and his strategy will be different from yours.” — Motley Fool, Nov 16, 2025

This context matters when judging him now.

His subsequent calls have been uneven: correctly identifying index concentration risks, but incorrectly timing shorts during the COVID rebound. Some positions expired worthless; others were early but directionally correct. The market remembers his successes, forgets his humanity, and rarely acknowledges how being right too soon is indistinguishable from being wrong.

He is not alone, either.

Jeremy Grantham, John Hussman, Mark Spitznagel — each carries the reputation of sounding alarms. These analysts occupy an uncomfortable space: they study excess, they warn early, they get mocked in the boom and vindicated in the bust. Markets celebrate optimism far more than skepticism.

But skepticism isn’t sabotage; it’s stewardship.

And Burry’s warnings today — particularly around AI valuations and capital flows — are less about calling a crash (or are a recession indicator) and more about pointing out a system straining under its own incentives.

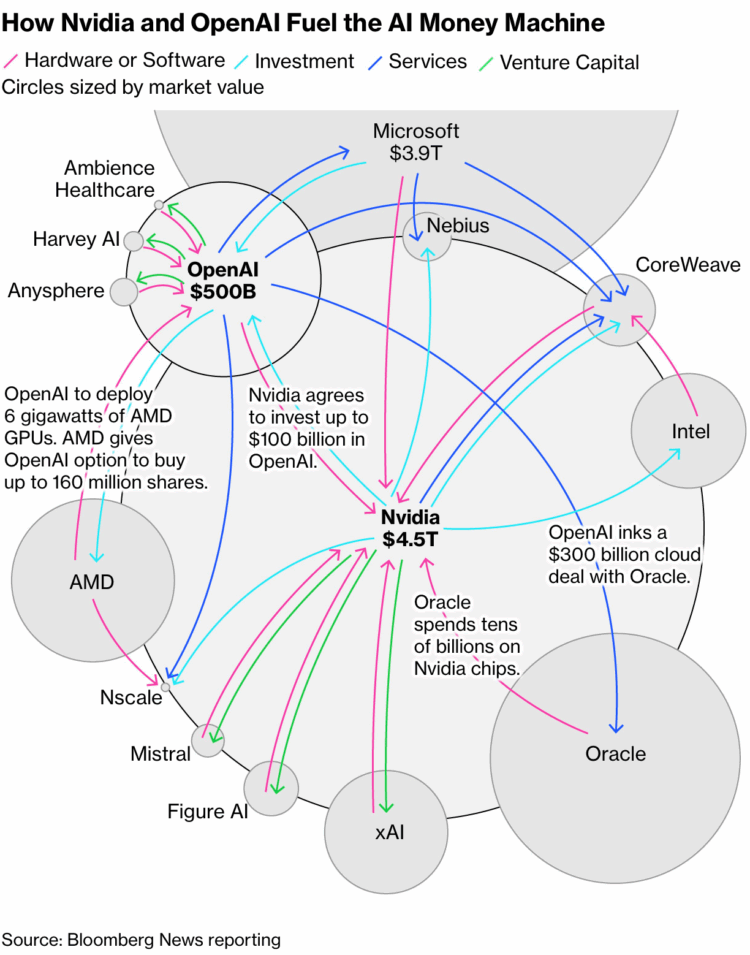

Movement II: The GPU Ouroboros, A Snake Made of Silicon

TLDR: The AI boom is powered (partly) by companies investing in and buying from each other, creating valuation momentum that looks like demand but often behaves like leverage.

The cycle has a computational heart.

The AI cycle’s heart is not just compute: it’s circular capital.

Unlike traditional value creation, where growth stems from customer adoption, product-market fit, or margin expansion, today’s AI megacaps have discovered a new gravity: companies funding each other’s growth, buying each other’s infrastructure, and reinforcing each other’s valuations.

Here’s how it works:

Nvidia invests in or strategically aligns with major AI labs.

Those AI labs raise billions from VCs and sovereign funds, some of whom hold large positions in Nvidia.

The labs spend enormous portions of that capital on Nvidia GPUs.

Nvidia recognizes revenue, boosts guidance, and its stock climbs.

Higher valuations make it easier to deploy more capital into AI ecosystems.

The loop continues.

It’s not fictional — it’s just unfamiliar.

And it differs from past cycles in three important ways:

The scale is unprecedented.

GPU capex at hyperscalers is measured in tens of billions annually.The asset life assumptions may be aggressive.

Wall Street models GPUs as 5–7 year assets.

Engineers whisper “2–3 years, realistically.”The revenue is real, but the demand is reflexive.

It’s driven by capital availability as much as customer need.

This is not illegal.

It’s not even irrational.

It’s simply a system feeding itself faster than fundamentals may justify, and investors deserve transparency on that distinction.

What’s “normal”?

In a textbook, supply increases when demand increases, revenue follows customer utility, and valuations rise on cash flow expectations. This flow follows a similar story arc with such repetition that its simply called ‘The Law of Supply and Demand’.

What’s happening now?

Supply increases because capital is cheap for a select group of firms.

Demand increases because AI labs are flush with investment dollars.

Valuations rise because the same capital inflates both producers and consumers.

We are not witnessing a scam, we are witnessing a feedback loop.

Movement III: The Case For Staying The Course

TLDR: Despite distortions, AI has real secular tailwinds and long-term investors historically outperform those who trade based on fear or prediction.

For all the skepticism (valid skepticism) the bull case is also strong.

AI (and talk of whether we are in a AI Bubble) is not a marketing gimmick; it is fast becoming a foundational infrastructure, akin to cloud computing in 2010 or broadband in 2000. Even if valuations correct, the underlying demand trajectory is real.

Here’s why the bullish argument remains compelling:

1. Compute demand still exceeds supply

Every major hyperscaler reports backlogs for GPU clusters stretching across multiple quarters. This is not speculative spending but reflects genuine constraints. Since 2020, with elevated personal computer purchases, the graphic processors have been lagging demand. The advent of AI (and the advancing cryptocurrency pricing) has led to increased demand for higher performant GPUs.

By 2030, analysts believe supply of GPUs may be up to 40% below demand.

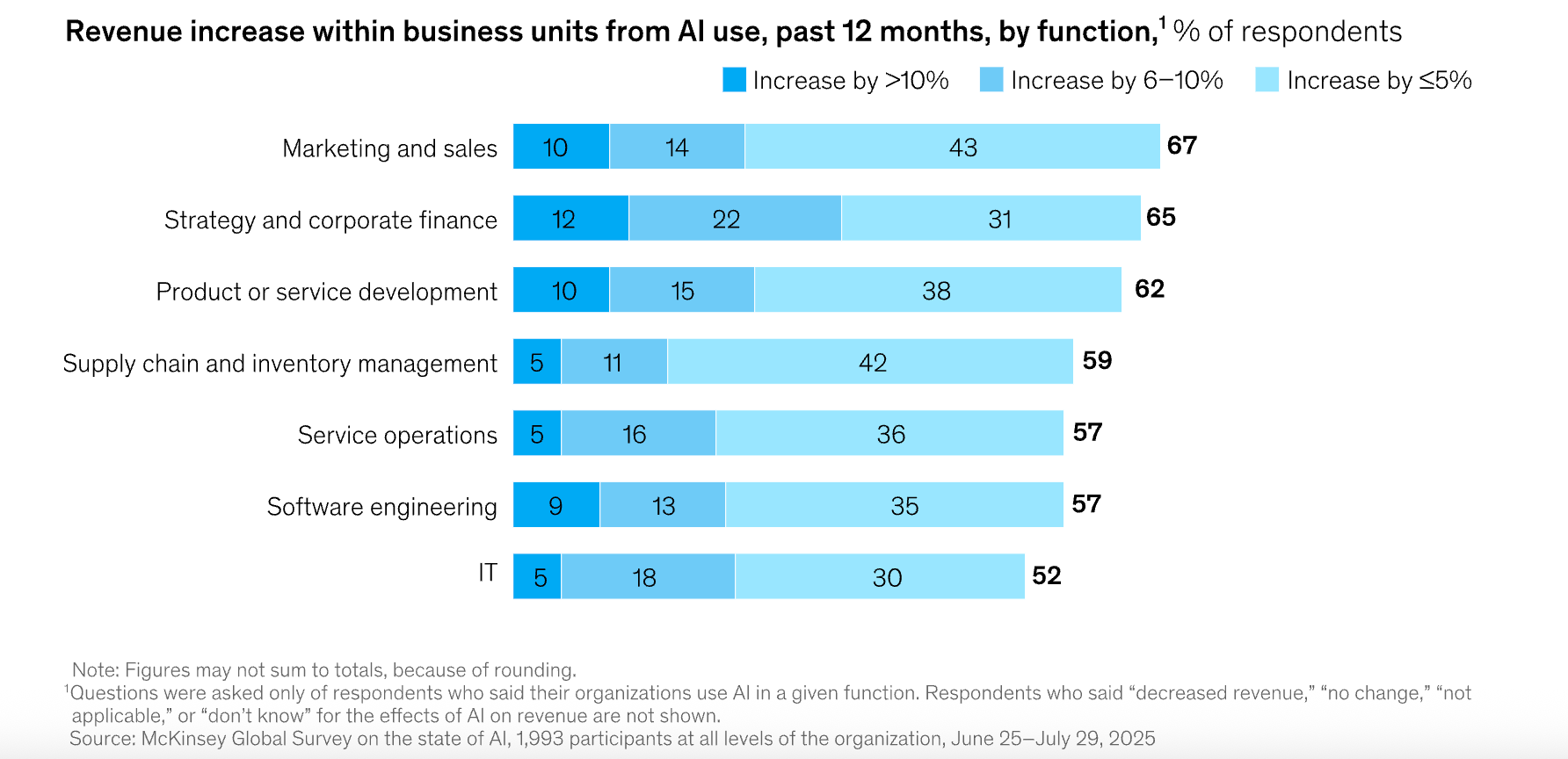

2. AI’s enterprise adoption is accelerating

What was once side experimentation is now embedded in cost structures, workflows, and product roadmaps. Companies are not dabbling; they are deploying. Mckinsey in their ‘The state of AI in 2025’ report found nearly 90% of commercial customers had deployed AI in at least one of their business functions.

3. Productivity gains could justify long-term multiples

If AI tools meaningfully reduce labor hours or elevate output, even partial productivity gains ripple through margins, GDP, and valuations.

4. Historically, secular tech cycles overshoot but do not reverse

The dot-com bubble burst, but the internet did not disappear — it expanded.

The cloud bubble inflated, but AWS, Azure, and GCP now dominate global IT.

However, spending during the onset of major technological development are a clear anchor to investors of where the titans of industry are going. This capital intensity towards infrastructure, though, has dampened and even constricted hiring — as reporting in Indie Investors last article: It Wasn’t the Robots: The Real Reason Jobs Are Declining in 2025

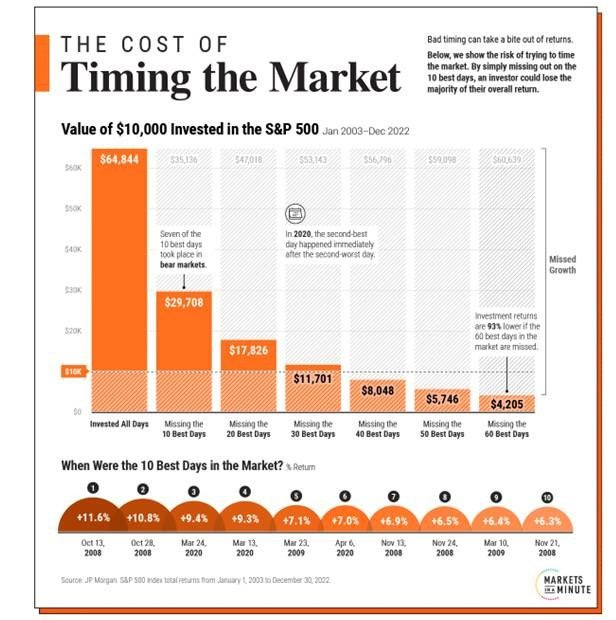

5. Long-term investors outperform.

The Motley Fool’s analysis — reinforced by multiple studies from JP Morgan and BlackRock — shows that missing even the 10 strongest market days in a decade can cut portfolio returns by half.

These days often occur in periods of highest fear.

This data argues for humility in timing market tops.

The system may be overheated,

but the story is only partially written.

Retail investors don’t have to choose between Burry’s caution and the bulls’ confidence. They can hold both truths simultaneously: valuations can be stretched and AI can have a multi-decade runway.

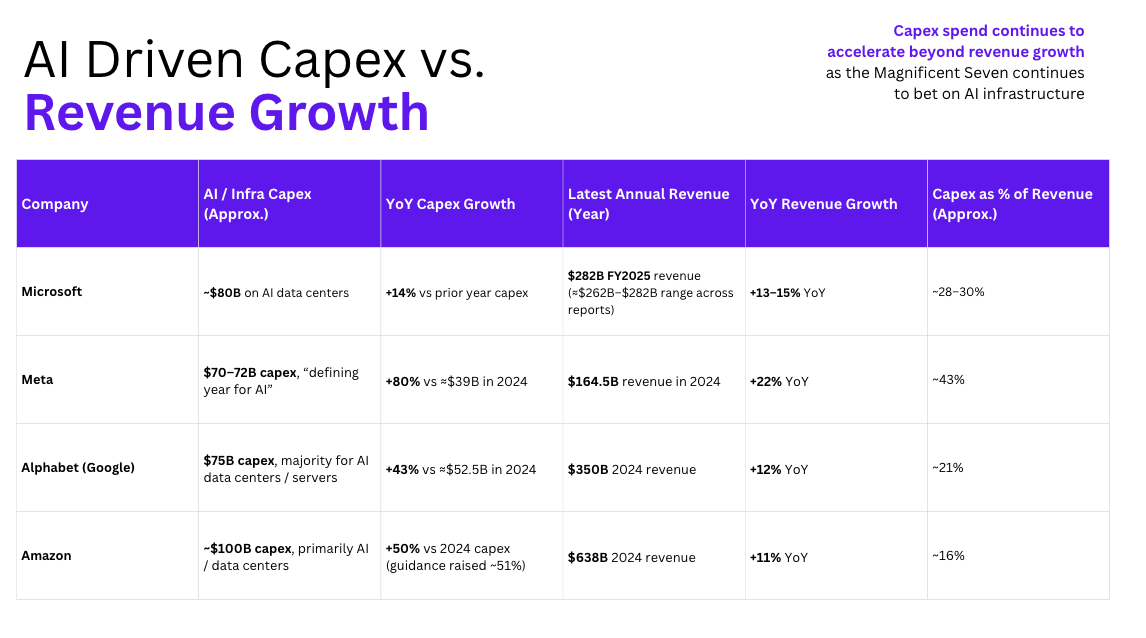

Meta’s 2025 capex is projected to almost double from 2024, while revenue grew about 22%. Business Insider+1

Alphabet is planning a 43% jump in capex to $75B, against roughly 12% revenue growth. DatacenterDynamics+2CFO Dive+2

Amazon’s 2025 capex guide (~$100B+) is set to rise about 50% while 2024 revenue grew 11%. DatacenterDynamics+2IO Fund+2

Microsoft is on track for tens of billions more in AI infrastructure spend, with plans exceeding $80B–$100B while revenue is growing in the mid-teens.

Finale: Why it Matters

TLDR: A grounded, practical guide for how to navigate a market shaped by circular capital, mixed signals, and legendary contrarians.

This section is your navigation kit: a distilled set of principles drawn from the tensions of this cycle as a retail investor strategy handbook.

1. Use Burry as a lens, not a lighthouse

His warnings highlight real imbalances,

but one legendary call doesn’t make him the metronome of every future cycle.

Study the reasoning, not the reputation.

2. Track circular capital (it’s a leading indicator)

When producers and consumers of GPUs are financially entangled,

valuation signals blur.

Tactical Checklist:

Compare revenue growth to unique customer growth

Track related-party investments

Examine depreciation assumptions on AI infrastructure

Watch for capex that grows faster than addressable markets

3. Avoid binary thinking — it’s how retail gets trapped

This is not “AI bubble vs AI revolution.”

It’s both. It’s layered. It’s nonlinear.

Build barbell portfolios:

Conviction long-term positions

Small protective hedges

Dry powder for dislocations

4. Remember: being early is being wrong (financially)

Skeptics often die on timing, not analysis.

If you short, define your horizon.

If you go long, define your thesis.

Never hold either indefinitely out of pride.

5. Side with compounding over clairvoyance

The data is overwhelming: those who stay invested, rebalance intentionally, and avoid panic outperform prediction-driven traders.

Tactical Move:

Automate contributions

Add incrementally during fear spikes

Review allocations on schedule, not based on headlines

6. Respect the real part of the AI story

Strip away excess, and a secular trend remains:

compute becomes cheaper, intelligence becomes embedded,

and the economy reorganizes around automated leverage.

Ignoring that because valuations are frothy

is as dangerous as ignoring froth because the tech feels magical.

7. Stay human in the data

Markets are systems.

Investors are people.

Your advantage is perspective, not omniscience.

Stay curious.

Stay grounded.

Stay open to both the fire and the fuel.