The Griswold Effect: How the Holiday Economy Makes Joy Expensive

A data-driven look at holiday spending trends, inflation, and why celebrating costs more each year

Prelude Poem: A Christmas Carol for the Modern Wallet

In the jolly-rush holidays,

when wallets feel thin,

The shoppers spilled out

with their carts to the brim.

They queued at the CVS,

cold drops, Vicks, and homeopathic drams.

While the flu-shot reminder

blinked bright overhead.

The storefronts were sparkling,

the markets were too,

All jingles and jangles

red-green-chart hue.

BNPL notes floated

like cheer from the shelf

A gift for today

from tomorrow-you’s self.

They swiped for nostalgia,

they swiped for the thrill

For the half-offs, vintage cast-offs,

delay that buy-now holiday bill.

But here’s the small wisdom

no influencer keeps:

Wealth doesn’t hide

where the tissue paper gets deep.

It’s found in the moments

you choose not to Yolo-spend,

And life that evolves and compounds

long after year-end.

So hold close what is priceless,

let the cheap things stay cheap

And build joy that pays dividends

even while you sleep.

Movement I: How Economic Uncertainty Changes the Way We Celebrate

TLDR: When the future feels foggy, people don’t spend less — they spend differently: more emotion-driven choices, more small luxuries, and more BNPL to preserve the holiday story.

The backdrop to this holiday season isn’t a snowglobe; it’s a flickering screen. The country is emerging from the longest government shutdown on record, airlines are still repairing their route maps after the Department of Transportation’s reduced service directives, and the labor market has begun to feel noticeably fatigued. Inflation has become uneven rather than consistently high or low, rising in one aisle and falling in the next. It’s a strange winter to summon holiday cheer.

A few numbers illustrate the tone;

Non-farm payroll growth is down more than 30 percent year over year.

Federal Reserve rates remain elevated at 3.7 to 4 percent, far above the near-zero lows of 2021.

Thanksgiving dinner was cheaper this year—down roughly 5 percent thanks to turkey prices falling nearly 15 percent—but core grocery prices are still up 3.2 percent year over year, outpacing broader commodity inflation.

The data paints a picture of an economy that feels uneven, unsteady, and difficult for consumers to interpret with confidence.

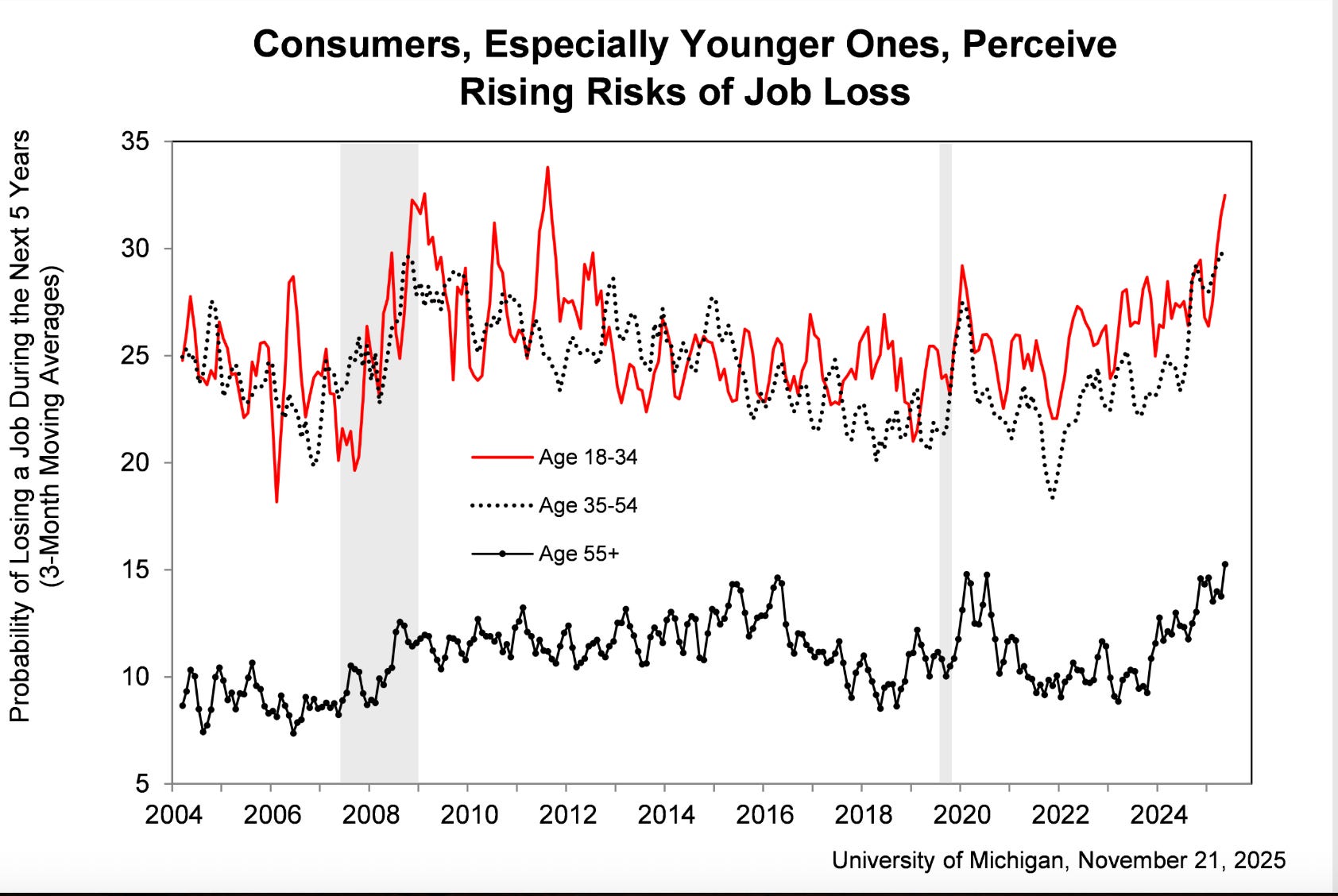

Unsurprisingly, sentiment has slipped. Surveys show rising economic anxiety, especially among younger Americans who increasingly treat job insecurity as a consistent companion rather than an occasional threat (see Indie Investors article on Job Trends). Many households are stepping into December with equal parts hope and hesitation, trying to build a holiday that feels familiar even while the economic weather turns unpredictable.

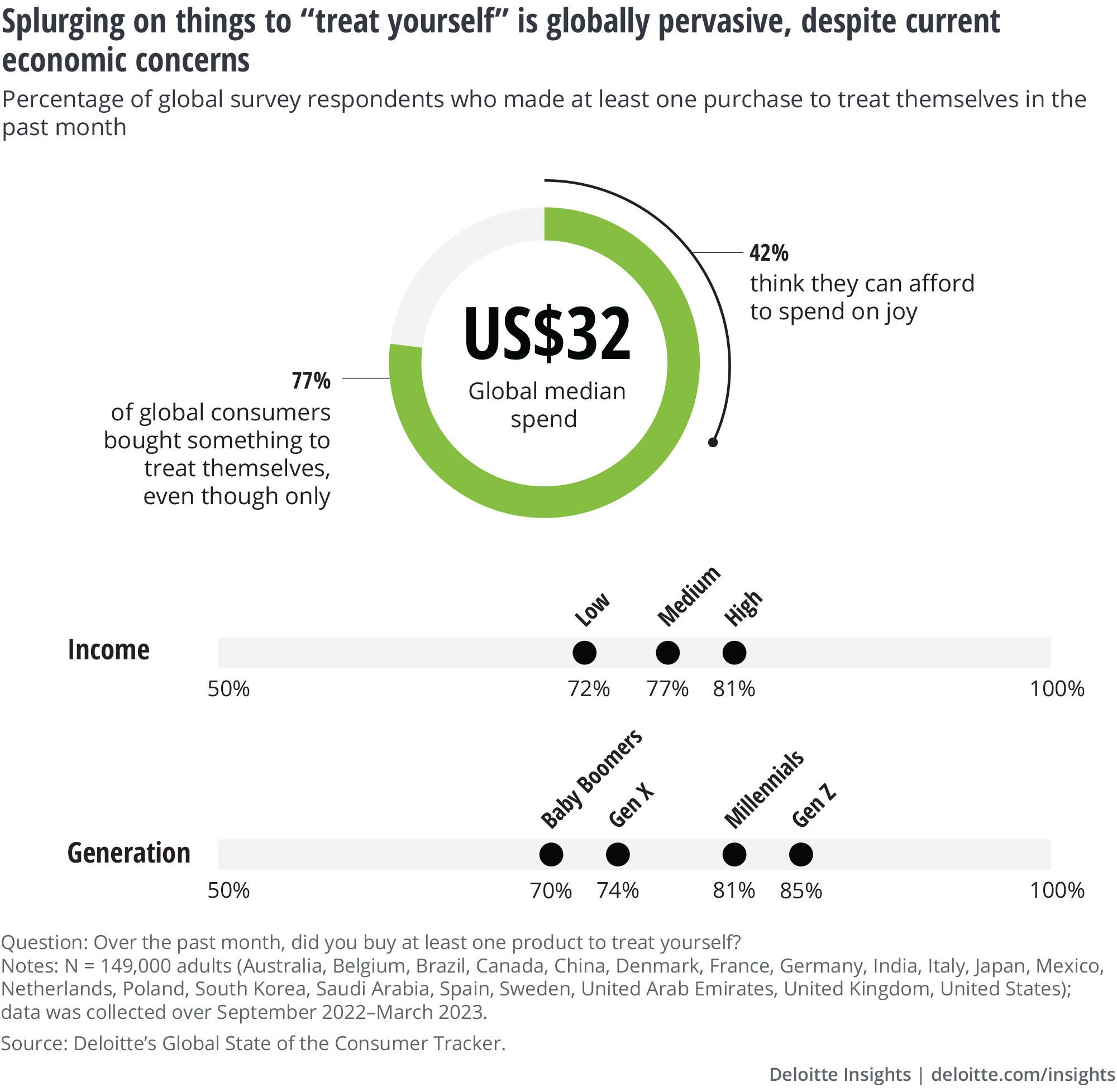

When people feel unsure about the months ahead, they rarely stop spending altogether. Instead, their spending shifts. They look for emotional footholds—small purchases that provide a sense of stability, comfort, or control. A spontaneous weekend trip can feel like a reset. A premium moisturizer or a winter coat becomes a self-affirmation. These aren’t extravagant splurges; they’re morale boosters, little moments that help people steady themselves against a foggy future.

Economists often describe this pattern as the Lipstick Effect: when macro conditions tighten, consumers reduce major purchases but increase spending on small luxuries. Net spending does not necessarily fall; instead, it spreads across a larger number of lower-ticket transactions. The thinking is simple: the year was hard, so let the holiday feel good.

The challenge is what happens when emotional spending blends with financial tools designed to delay the impact. Buy-now-pay-later platforms make it easy to convert today’s comfort into tomorrow’s obligation. The financial burden does not disappear; it simply arrives later.

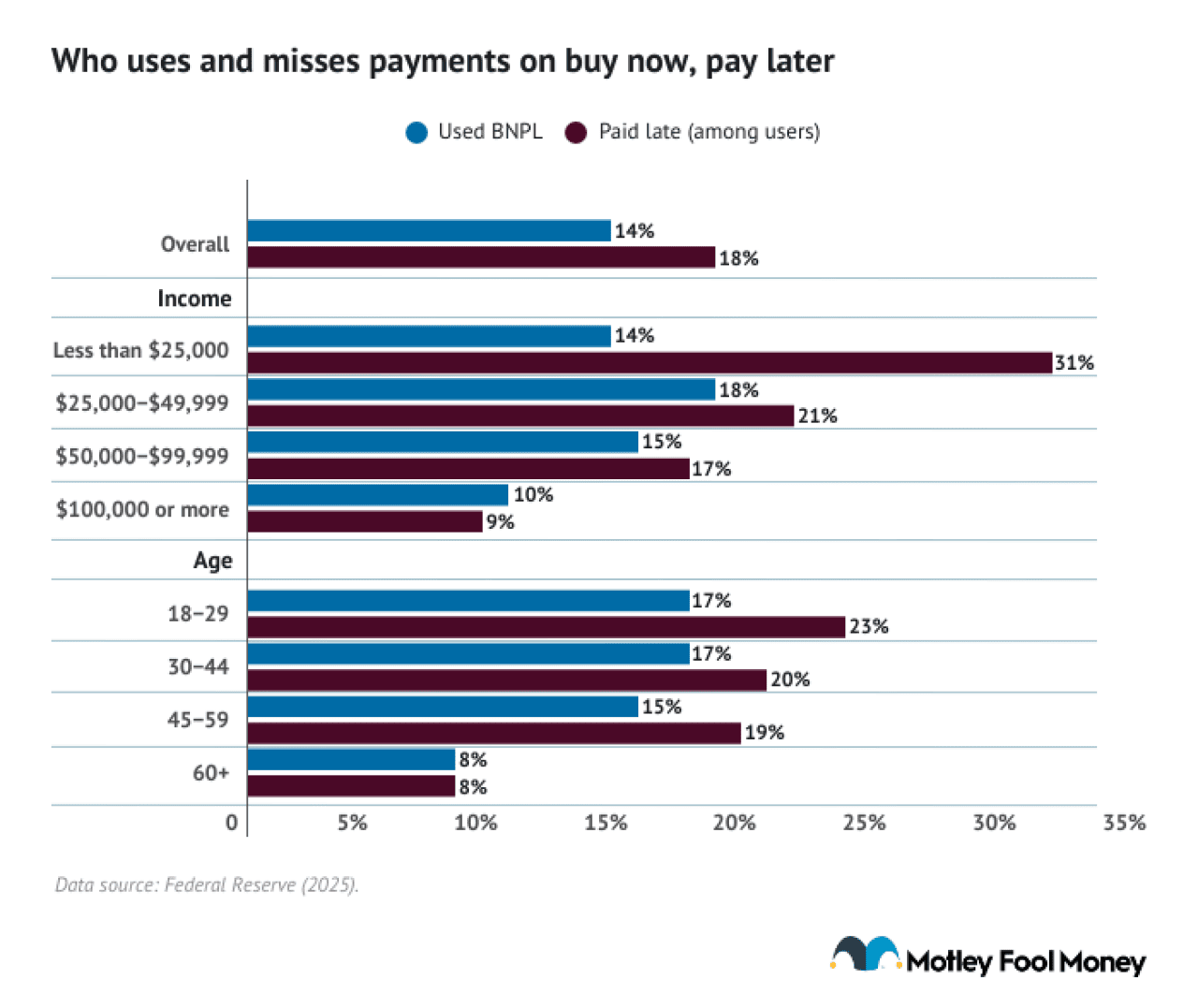

The data on late BNPL payments underscores the fragility. Thirty-nine percent of Gen Z users missed at least one BNPL payment last year, compared with about 12 percent for credit cards. Thirty-five percent of Millennials also reported missed payments. Borrowers with sub-580 credit scores now represent almost half of BNPL originations, and their default rate reached 3.5 percent in 2022. The overall BNPL default rate, at 1.9 percent, is significant given how aggressively these products are marketed as frictionless.

These loans don’t stay isolated. Companies like Klarna and Affirm bundle them into investment instruments and financial products. A fragile consumer base turns into a fragile asset class, creating risk that extends far beyond the holiday season.

So what should we make of rising holiday spending this year? Higher spending doesn’t automatically signal optimism. It often reflects emotional economics—the instinct to reclaim normalcy in an abnormal year. When people spend instead of investing, it can indicate caution about the future. When they spend in familiar patterns despite the noise, it can indicate resilience. Either way, spending today is being guided less by prices and more by what people believe the next few months might bring.

Uncertainty shapes why we shop, and expectation inflation shapes how much ends up on the credit bill.

Together, they are rewriting the psychology of the holiday season. Beneath the lights and music, people aren’t just buying gifts—they’re trying to buy a sense of steadiness in a winter that does not feel entirely steady.

Movement II: Why the Holidays Quietly Get More Expensive Every Year

TLDR: Holiday budgets inflate due to subtle expectation creep: traditions expand, social comparison raises the bar, and families unintentionally add without subtracting.

Holiday traditions tend to grow the way storage bins do: quietly, steadily, and a little more each year. Rituals stack on top of one another as households try to recreate the feeling of holidays past while adding something “special” for the present. Chestnuts need roasting, fireworks must be bought, a wreath becomes a second wreath.

What begins as sentiment gradually becomes maintenance, and then expectation. It is a pattern that feels borrowed from Silicon Valley’s endless cycle of iteration, or Wall Street’s quarterly push for growth, but it unfolds just as easily in a suburban living room. The impulse is the same as Cindy Lou Who’s mother trying to win the Christmas light contest: elevate, expand, impress — and outdo last year’s version of yourself. The result is a slow-moving escalation that raises the cost of “normal” year after year.

Social pressure accelerates this drift. Festive spirit does not make us immune to comparison; if anything, the holidays concentrate it.

Social media quietly resets the visual baseline of what a “proper” holiday looks like. Instagram and TikTok feeds fill with tutorials on how to make a home look cozier, brighter, more curated — complete with “Top Amazon Finds for Holiday Hosting” and lists of must-have seasonal décor. Matching energy, once a feel-good mantra, has evolved into a far more aggressive consumer trend.

According to a Sprout Social survey, 80 percent of shoppers plan to use social platforms as much or more than last year to discover gifts, décor, and party essentials. Discovery turns into desire, and desire turns into obligation.

Some of this is timeless. People have always equated generosity with price, especially during the holidays. When the year has been difficult, that instinct intensifies. Hard times become a justification to stretch, not scale back. “This year was tough, so the holiday should feel big” is a sentiment as old as retail itself.

Where budgets fall apart is at the very beginning. Families often set expectations first — what the holiday should look like, what gatherings they will host, how many events they will attend — and only afterward consider the financial impact. By then, the emotional blueprint is already locked in. Expectations inflate faster than wages or savings, leaving households on the back foot as they enter the most expensive stretch of the year. Overspending becomes less about impulsive decisions and more about the quiet drift of tradition, obligation, and comparison. People are not acting recklessly; they are making intentional choices that simply run ahead of their financial reality.

This drift is subtle. Nobody decides that a holiday dinner should become a feast, or that decorations should multiply. It happens gradually.

A new centerpiece one year becomes the baseline the next. Garland that once felt extravagant becomes the starting point. Each addition becomes part of the standard, and the standard steadily grows more expensive without anyone acknowledging the shift.

Movement III: The Micro-budget Method. A Holiday Budget You’ll Actually Follow

TLDR: Vague budgets fail; micro-budgets win. Small, specific spending buckets stop leaks, reduce impulse buys, and make December financially sane.

The traditional budget is not working under the burden of the holidays cheer. Gifting may work as a budget category during a normal month, but when Amazon delivery notifications and target carts are packed you need to get more granular.

Then you have the hidden categories including wrapping, shipping, holiday travel meals, new outfits, might as well add a hoo roast beast. Then it paints the picture as to why Americans on average underestimate their holiday spend by 20-30% each year.

By setting up smaller budget categories (a Microbudget), then you can exhibit more control during your holiday.

Break down spending into subcategories:

Gift spending per person

Travel + Meals

Holiday clothing/include seasonal clothing

Host gifts/stock stuffers

Charitable giving

Events/secret Santas

Deck the halls holiday decor

Wrappings and disposable items

“Forgot something” fund

Think of these categories not as fences but as completion steps to deck the halls. You got your decor, your wrappings, and your gifts set. These boundaries reinforce your budget but also add a sense of accomplishment as you progress thorugh your holiday season. Then you also lose the temptation to pursue BNPL schemes as you have defined limits within your budget to support all the holiday cheer you have planned.

Some other practical tips:

Santa creates a list, so can you. Create a list for gifts before Black Friday or sales pop up to limit the FOMO

Allocated a fixed budget and check as you are navigating shopping your progress against those categories

The purpose is not to limit the joy during the holiday season, but it clarifies it. Its easier to control spending and the holidays when you put every dollar to work during the holiday. Specificity can be the antidote to the winter storm of holiday spending.

Finale: The Indie Investor Holiday Field Guide

TLDR: Spend intentionally, design December around meaning, cap drift, and choose joy that doesn’t send you into January on your heels.

The last few sections point to a simple truth: holiday overspending rarely comes from impulse. It comes from emotional economics, tradition drift, and expectations that quietly outrun budgets. A good holiday doesn’t need more money; it needs more intention. The field guide below distills the practical takeaways.

1. Start with the anchor, not the aspiration.

Define your holiday budget before defining your holiday traditions. Let the financial frame shape the plan, instead of forcing the plan to bend the frame.

2. Rebalance your “holiday portfolio.”

Prioritize high-ROI experiences — time spent together, meaningful gestures, shared rituals — over low-ROI purchases like filler gifts and obligatory extras. A holiday budget works best when it’s diversified toward emotion, not volume.

3. Put a ceiling on tradition creep.

Limit the number of events you’ll host or attend. Set boundaries for décor upgrades or “just one more thing” purchases. Drift fuels overspending more than spontaneity ever will.

4. Use microbudgets to give every dollar a job.

Break your holiday spending into specific categories: gifts per person, travel meals, holiday clothes, charitable giving, hosting supplies. Clear buckets eliminate the leaks that derail December.

5. Write your BNPL rules before December starts.

Decide when and why you’ll use buy-now-pay-later, if at all. The decision made in calm moments often protects you from emotional borrowing.

6. Build a small “joy buffer.”

Set aside a tiny cushion for spontaneous fun — the unplanned coffee catch-up, the last-minute cookie swap, the small luxuries that brighten the month. A little cushion prevents large detours.

7. Ask the one Indie Investor question.

Will January me be proud of this?

It’s a filter that keeps holiday joy compounding instead of accumulating interest.

Sources:

Sundby, Alex. “Duffy says travel could be ‘reduced to a trickle’ ahead of Thanksgiving if government shutdown continues.” CBS News, 10 Nov 2025. https://www.cbsnews.com/live-updates/canceled-flights-government-shutdown-airlines-scramble/ CBS News

U.S. Department of Agriculture, Economic Research Service. “Food Price Outlook: Summary Findings.” ERS (USDA), latest release. https://www.ers.usda.gov/data-products/food-price-outlook/summary-findings Economic Research Service

University of Michigan, Survey of Consumers. “Home Page.” SCA (School of Business). https://www.sca.isr.umich.edu/. sca.isr.umich.edu

Deloitte Insights. “Understanding splurge spending: Inflation, the Lipstick Index, and this holiday consumer.” Deloitte, 2025. https://www.deloitte.com/us/en/insights/industry/retail-distribution/consumer-behavior-trends-state-of-the-consumer-tracker/splurge-spending-inflation-lipstick-index.html