The New American Dream Is Leveraged, Just Not Where You Think

On mortgages, market access, and the quiet rules that shape who gets to build wealth

Prologue: The New American Down Payment

We are taught early

that safety has an address.

Thirty years,

Fixed rate,

A door that locks behind you.

Credit is extended for walls,

for roofs,

for a future you can photograph and frame.

But not for ideas.

Not for companies that breathe before they scale.

Not for the risk of becoming early instead of settled.

A home may fall in value.

A neighborhood may hollow.

Interest rates may turn the math upside down.

Still, we call it prudent.

Markets, meanwhile,

are framed as weather.

Unpredictable,

Dangerous even, to step into unprepared.

The modern dream is collateralized.

Risk is permitted only when it looks like tradition.

A house can fall in value.

A market can rise for decades.

Yet only one is framed as reckless.

Capital compounds.

Ownership scales.

But only one dream

is worth the leverage.

Movement I: Access Exists. Control Does Not.

TLDR: Crowdfunding is legally accessible, but institutional constraints, especially within brokerage and retirement accounts, limit real participation. Access exists in theory, not in practice.

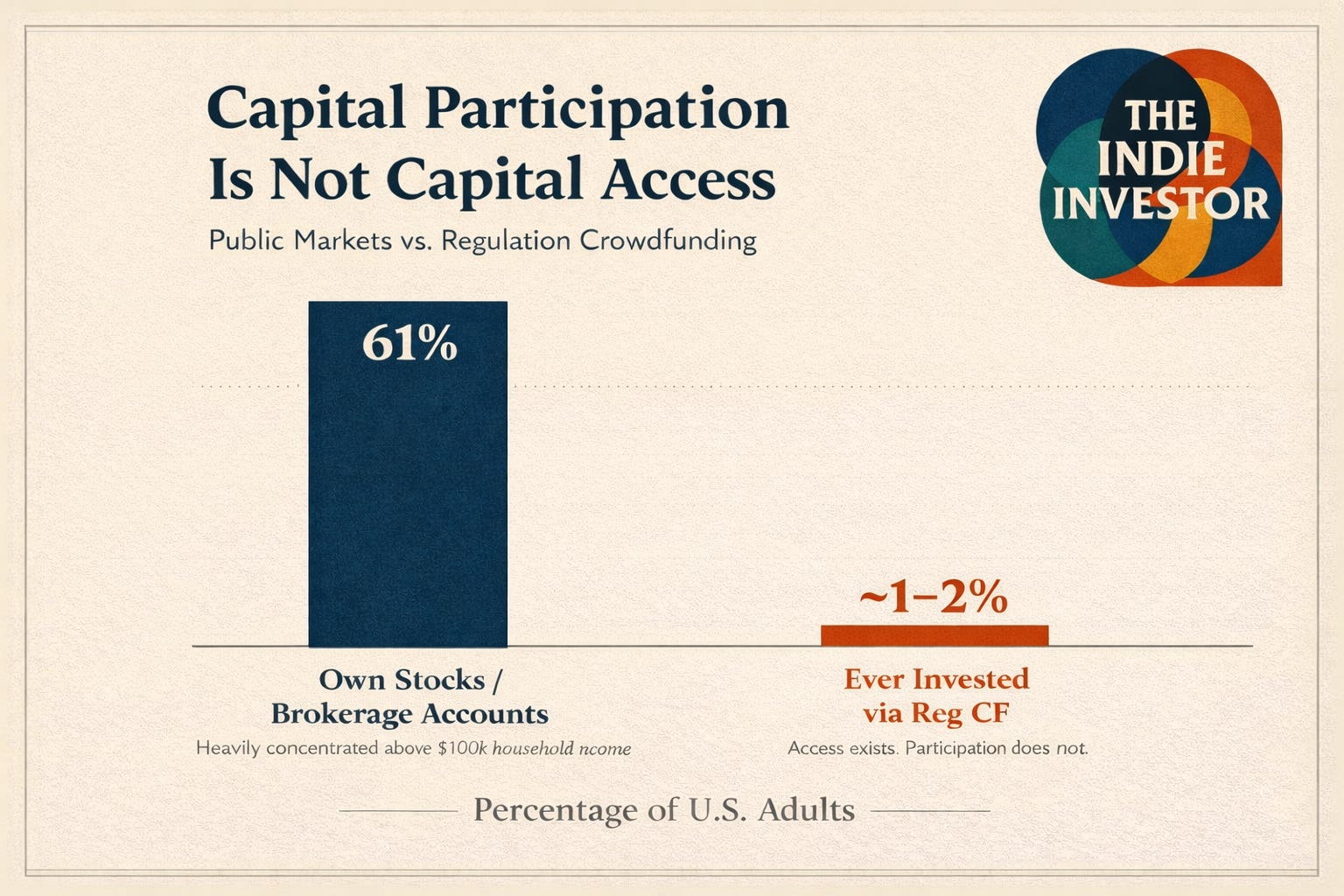

Equity crowdfunding has been legally viable in the United States since 2016, yet its adoption remains marginal relative to public markets. Today, platforms like WeFunder, StartEngine, and Republic collectively report millions of registered users, but actual investor participation remains thin when compared to brokerage account ownership.

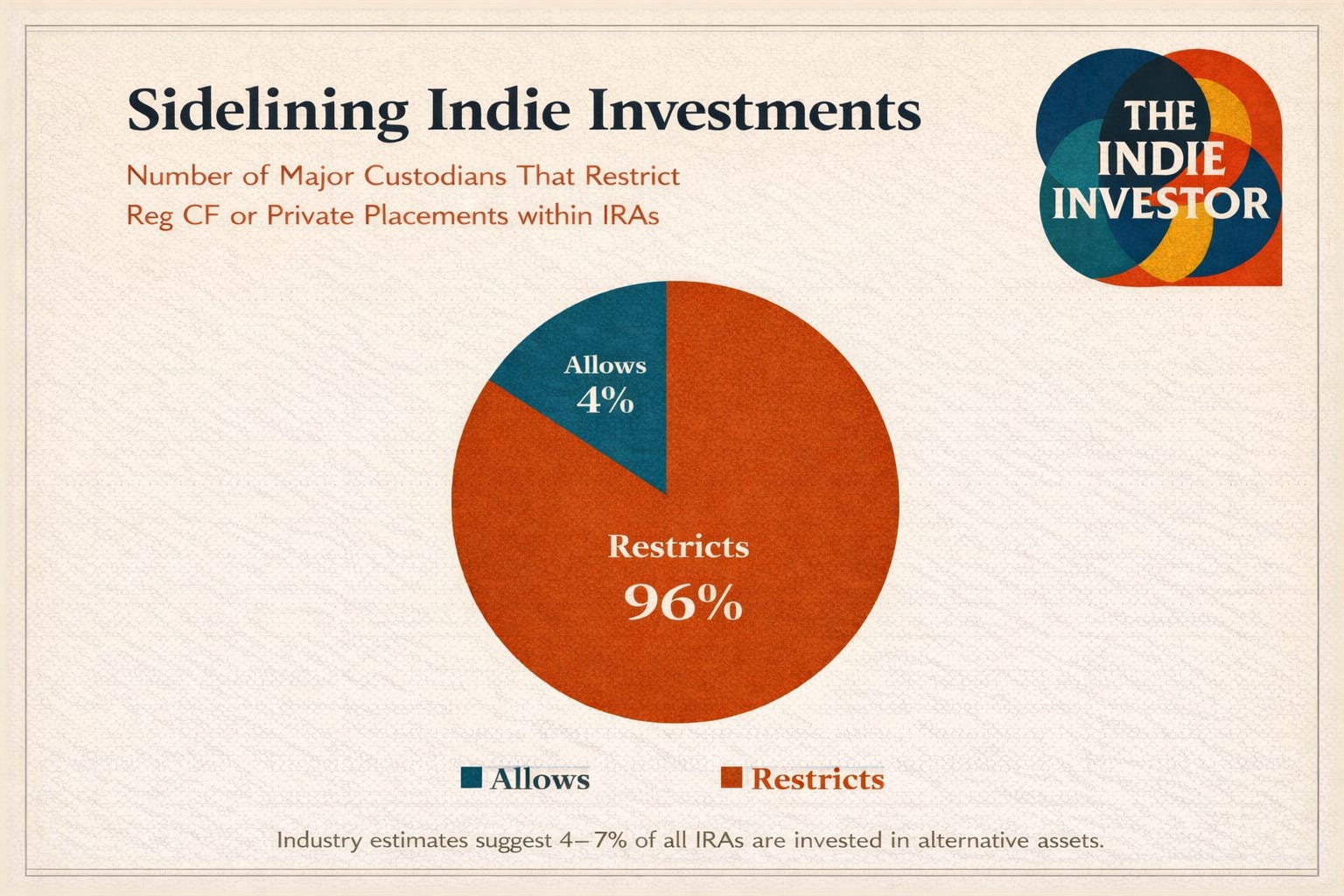

The bottleneck is not interest. It is infrastructure. In practice, many investors encounter friction not at the platform level, but within their own financial institutions. A recent case made this visible: an investor with a large brokerage relationship and a so-called self-directed IRA attempted to invest in a crowdfunded company, only to discover that private placements were functionally excluded. “Self-directed,” in this context, meant choosing among pre-approved public instruments, not directing capital freely.

This is not an edge case.

The language of access exists, but control remains tightly scoped. The result is a system where opportunity is technically legal yet practically unreachable for a large segment of retail investors.

Movement II: Risk Is Not the Barrier. Familiarity Is.

TLDR: The issue isn’t risk, but who controls it. If institutions can package and profit from it, it’s allowed—if not, it’s restricted.

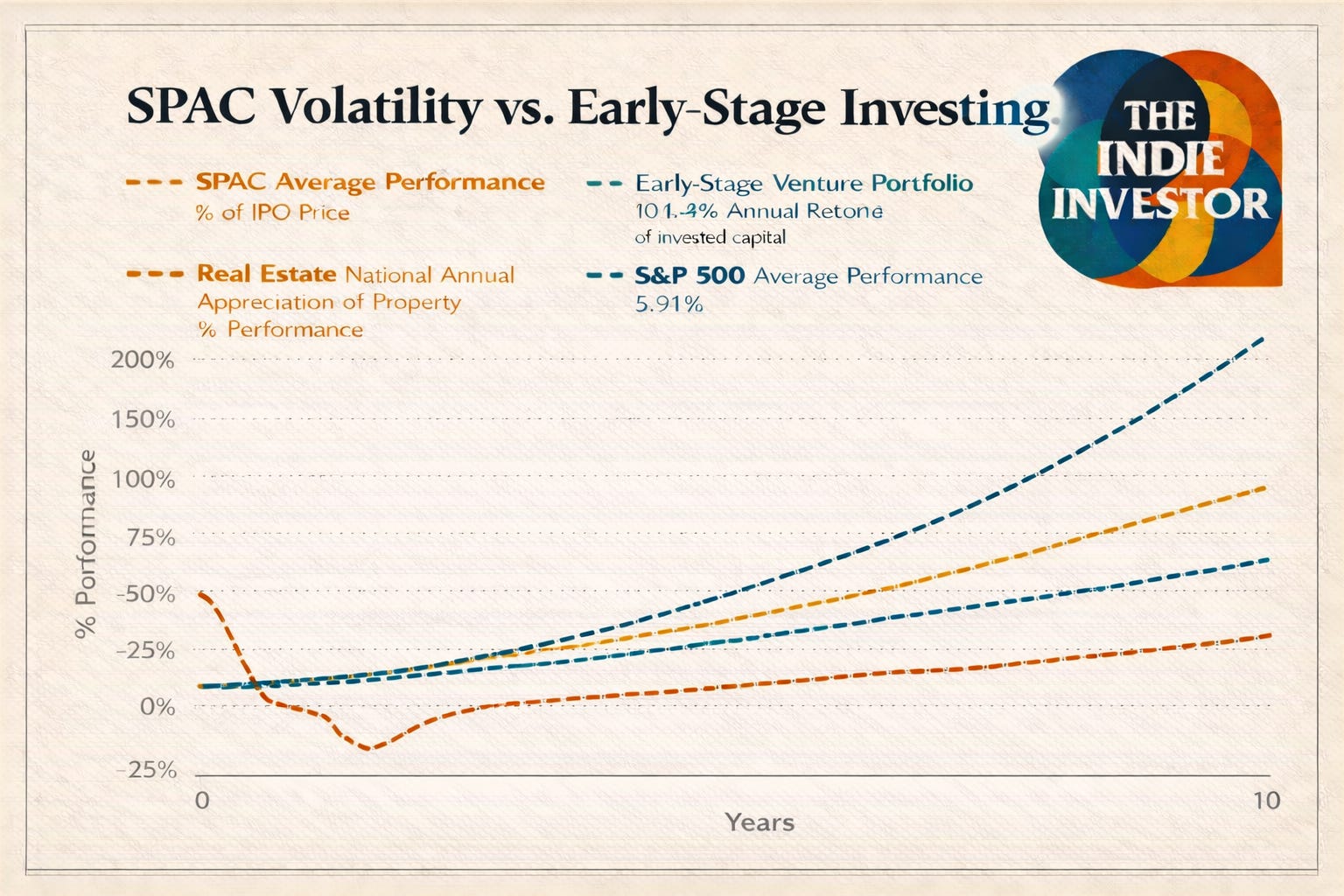

Financial institutions often frame these restrictions as risk management. The narrative is protective: shielding retail investors from speculative assets. Yet this framing collapses under comparison. The same platforms that restrict early-stage private investments routinely allow access to SPACs, leveraged ETFs, options trading, and increasingly, prediction markets.

Consider the data:

Risk, clearly, is not disqualifying. What differs is standardization. Public instruments are legible, tradable, and easily intermediated. Private investments are not. They resist automation, they limit fee extraction, and they require institutions to relinquish a degree of narrative control over outcomes.

The question shifts, then, from “Is this too risky?” to “Who controls the rails?” When risk can be packaged and resold, it becomes acceptable. When it empowers individuals to behave like allocators rather than consumers, it becomes something to constrain.

Movement III: Why Housing Is Sacred and Markets Are Suspect

TLDR: Housing is treated as safe despite its concentration risk, while diversified market participation is framed as speculative; revealing a systemic bias in how risk is defined and permitted.

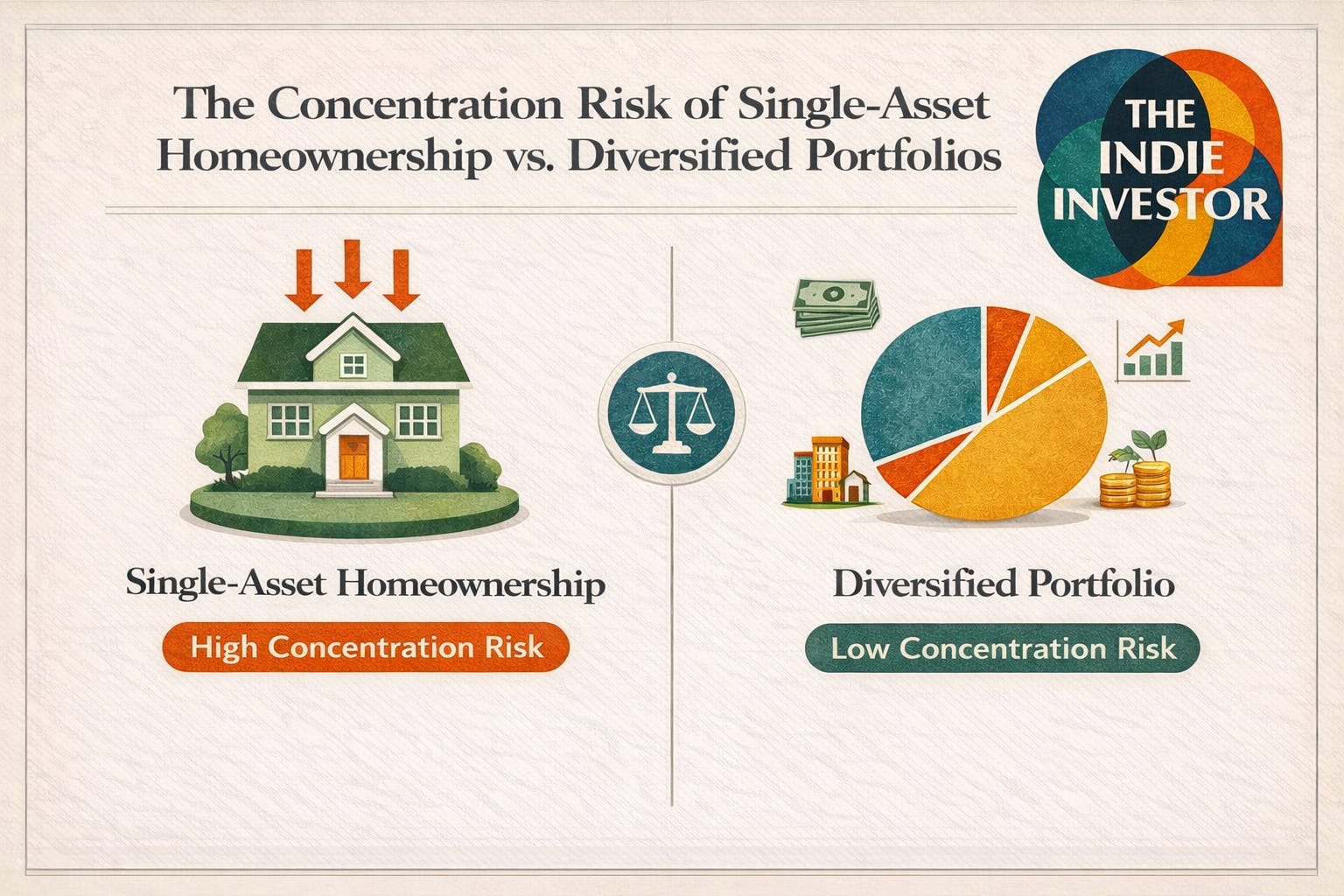

The United States has normalized leverage in one domain above all others: housing.

Mortgages routinely exceed six figures, are underwritten with long time horizons, and are culturally framed as responsible or even virtuous. Meanwhile, borrowing to invest in diversified markets or early-stage companies is treated as speculative and outright irresponsible.

It begs the question of why is it unacceptable for ownership in the systems that increasingly define economic mobility? Historically, housing has been treated as both a financial instrument and a moral one, a sanctioned way to take risk under the guise of stability. Yet housing is a single, illiquid, geographically concentrated asset, exposed to interest rates, local policy, and demographic shifts.

Yet the numbers tell a different story.

Homes fluctuate. Neighborhoods reprice. Interest rates reset. Still, real estate is canonized as stability, while markets are cast as casinos. This bias is cultural, not mathematical. Companies like Basic Capital expose the contradiction by applying mortgage logic to market participation: long-duration capital, structured repayment, and individual choice over deployment.

This framing lingers from an era when homes anchored communities and markets felt distant. Today, economic mobility is increasingly shaped by ownership in systems rather than proximity to property. The mismatch is not theoretical. It shows up in who builds wealth, who compounds early, and who remains perpetually late to participation.

The question, then, is not whether individuals can handle risk. It is whether institutions are willing to loosen their grip on where risk is allowed to live.

Finale: The Indie Investor Field Guide

A short compass for navigating what is actually happening beneath the language of access:

1. Audit your “self-direction.”

If your account cannot access private placements, Reg CF investments, or alternative assets, it is not self-directed. It is selectively permissive.

2. Follow the custody, not the marketing.

The real constraints are rarely on the investment platform. They live with custodians, compliance frameworks, and what institutions are willing to operationalize.

3. Distinguish volatility from denial.

An investment being risky is different from an investment being unreachable. One is a personal decision. The other is structural.

4. Question which risks are normalized.

Ask why leverage is celebrated in housing, tolerated in public markets, and restricted everywhere else.

5. Optimize for access before optimization.

Returns compound. Access compounds earlier. Without the latter, the former is theoretical.

The future of investing is not about eliminating risk.

It is about deciding who gets to choose it.

And whether the American Dream remains a house with an address,

or expands into a portfolio with agency.