It Wasn’t the Robots: The Real Reason Jobs Are Declining in 2025

Amid the hype around AI layoffs, the real disruptor has been the cost of money and the encoded message behind it.

Prelude: The Illusion of the Machine

They told us it was the robots.

That metallic hands had taken the wheel,

a silent reorganization replacing teammates with silicon.

But look closer.

The layoffs weren’t born on source code or a lab;

they were written in Fed minutes and antiquated C-Span transcripts.

While headlines screamed “AI eats jobs,”

the bond markets whispered a quieter truth:

borrowing money got expensive again.

That’s the real automation — interest rates pressing pause on ambition.

Not code, but cost, deciding who stays and who goes.

The Indie Investor isn’t a finance column. It’s a movement in verse: a dialogue between money and meaning, between markets and the people moving through them.

Movement I: The Narrative vs. The Numbers

TLDR: AI didn’t take jobs. Rates did. Which means the real arbitrage isn’t in code but in credit. The Indie Investor sees tightening not as tragedy, but as timing.

Everyone blamed the robots.

Tech companies spent 2025 talking about “AI efficiency” while announcing thousands of layoffs. But beneath those headlines was the real story — money got expensive.

When capital costs rise, companies don’t innovate; they consolidate.

They call it efficiency, but it’s really defense.

Instead of betting on new ideas, firms protect their balance sheets by hoarding cash, freezing hiring, shelving R&D.

And you can see it everywhere:

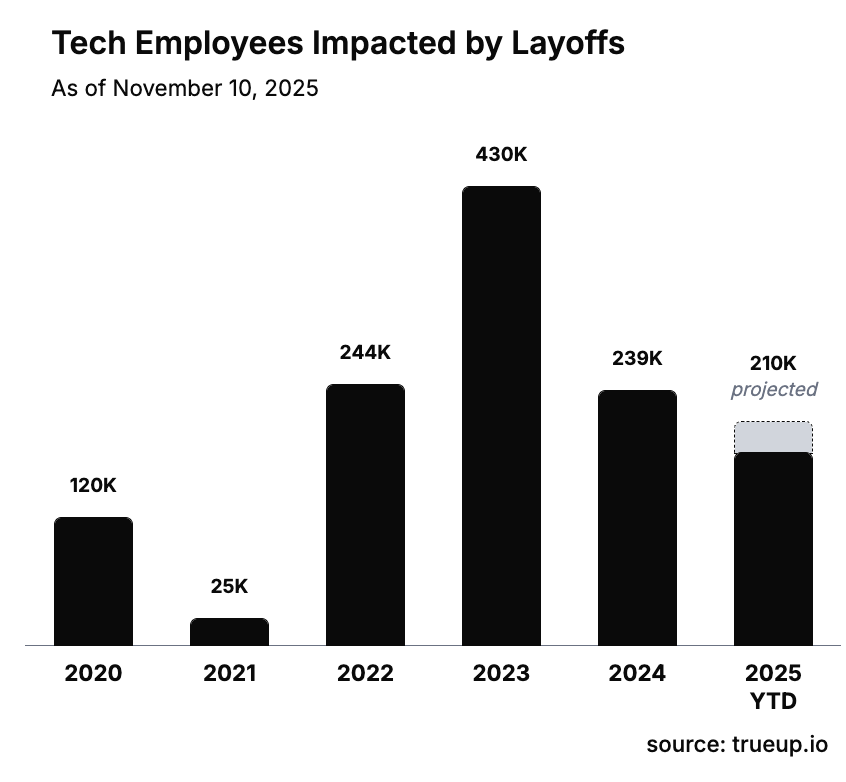

Layoffs are up year-over-year across tech, finance, and manufacturing.

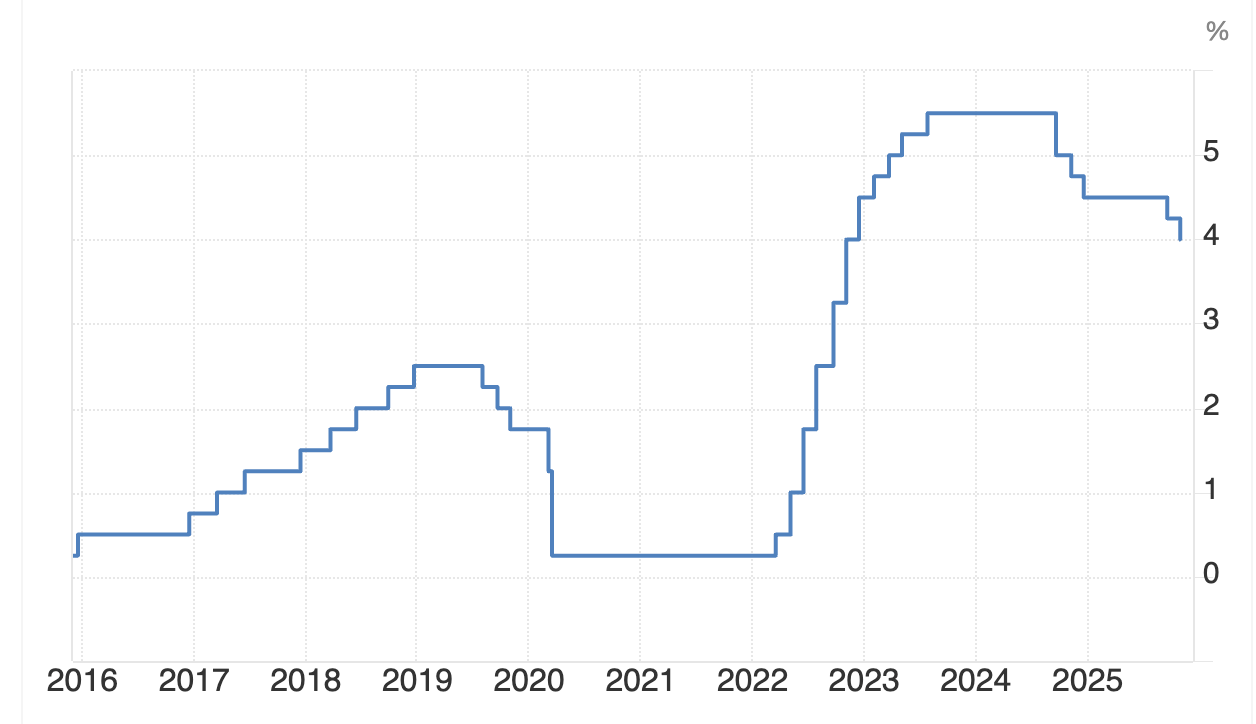

The Fed has kept rates elevated since mid-2022 to cool demand and inflation.

Innovation budgets have shrunk: the first casualty of expensive money.

When capital tightens, curiosity contracts.

Those still employed are behaving differently too.

A CBS report showed a 25 % drop in job switching among workers with under four years of tenure. Fewer people are moving means fewer new ideas and slower wage growth. Companies gain “efficiency,” but lose circulation. The economy gets leaner, not livelier.

The Fed designed it that way. Raising rates is how it tests the pulse of demand — slowing hiring, spending, and ambition until inflation cools but recession doesn’t ignite. It’s monetary tightrope walking.

Pull up the charts — as Fed rates rose, layoffs climbed almost in sync.

Tech led, but finance, logistics, and manufacturing followed. The cause wasn’t automation. It was austerity.

From job numbers to fed rates, you can see a visual correlation — as rates went up, layoffs in tech (but also consistent across finance, manufacturing, and other industries) also increased.

Then where is the connection to AI for job certainty?

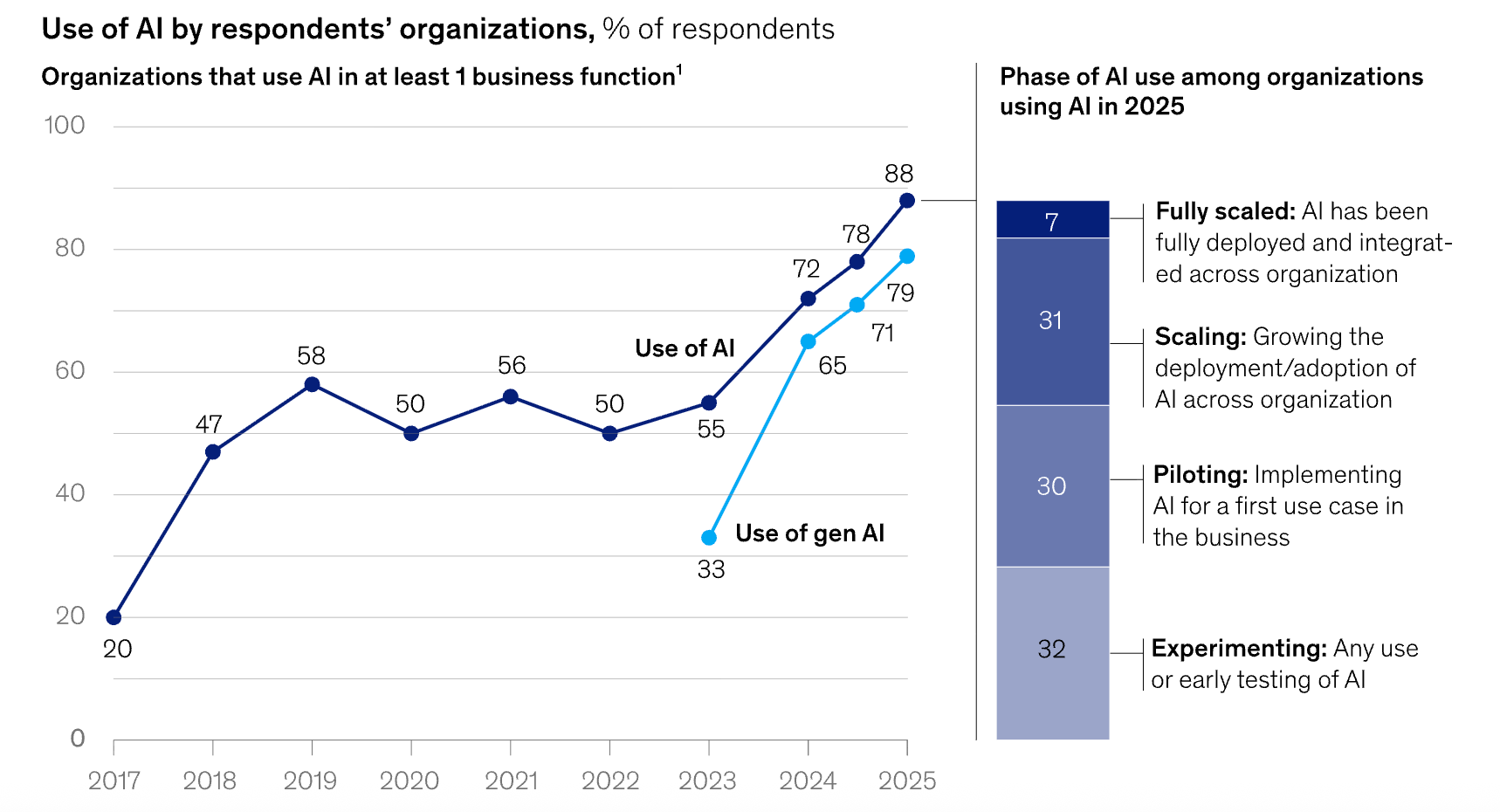

Thats where the data doesn’t support that headline. AI has been used in the majority of organizations since 2019 (with at least 1 business function utilizing AI). 2023 with the release of ChatGPT by OpenAI accelerated this adoption, however its growth doesn’t appear to correlate to the job numbers that are supposedly intertwined.

So where does AI fit?

It doesn’t — at least not in the way headlines claim.

AI adoption has been high since 2019, with most organizations using some form of automation in at least one function. The launch of ChatGPT in 2023 accelerated experimentation, but the timing doesn’t line up with the job cuts. The growth curve of AI use doesn’t match the decline in hiring.

So what’s happening?

We confused correlation with causation.

AI is visible. Rates are invisible.

And when the story and the stats diverge, that gap becomes an opportunity.

When markets don’t make sense, they’re usually telling you where the alpha lives.

Movement II: Catch these (Feds) Invisible Hands

TLDR: AI does not (yet) dictate hiring budgets, but Monetary policy does.

Every time the Federal Reserve releases its minutes, the market holds its breath.

For most people, those headlines feel distant — abstract phrases about “cooling inflation” and “restricting demand.”

But to anyone running a business or investing in one, those sentences are choreography.

Because when the Fed raises rates, it doesn’t just slow borrowing.

It slows belief.

The Cost of Confidence

Since mid-2022, the Federal Reserve has kept the benchmark rate above five percent, the highest level in over two decades.

The stated goal: curb inflation by reducing demand.

The real effect: restrain the appetite for risk.

High rates ripple outward like invisible hands, touching every decision point in the economy:

Hiring: When debt is expensive, companies delay expansion. The cost of new talent is treated like a liability, not an investment.

R&D: Innovation budgets shrink because the time horizon to return capital lengthens.

Venture and private equity: Deal flow slows as hurdle rates rise.

Startups: With credit tighter and valuations compressing, founders move from bold to cautious.

Even outside the U.S., the same rhythm applies.

In Europe, the ECB’s parallel tightening has cooled cross-border lending and early-stage funding.

In emerging markets, dollar strength squeezes liquidity and inflates import costs.

The Fed sets a tempo that others must follow, willingly or not.

The Federal Reserve doesn’t just shape interest. It shapes imagination.

How Policy Becomes Practice

Here’s the quiet chain reaction that headlines skip:

Rates rise: the cost of debt for companies increases.

Spending freezes: CFOs reclassify innovation as “non-essential.”

Hiring pauses: Managers hold back on offers, anticipating a slower market.

Market multiples compress: Equity values fall, and compensation tied to stock options becomes less attractive.

Consumer confidence dips: Demand softens, and growth narratives lose their music.

This is how a two-sentence update in a Fed statement becomes a six-month chill across sectors.

It’s not conspiracy; it’s conduction.

Monetary policy is the economy’s nervous system, and every rate adjustment is a signal to pull back or press forward.

The Global Context

Central banks are now in a synchronized slowdown.

The OECD reports that business investment growth has dropped to its lowest level since 2015, while global R&D spending declined in real terms for the first time since the pandemic.

This isn’t a failure of innovation; it’s a reflection of constraint.

Even governments that want to invest — in climate tech, semiconductor re-shoring, or digital infrastructure — must do so within higher borrowing costs. Fiscal optimism meets monetary restraint.

That tension defines the 2025 market.

And it’s where the Indie Investor finds opportunity.

Movement III: The Mirage of Efficiency

TLDR: Executives are under pressure from boards, investors, and the Street itself.

In 2025, Bloomberg Intelligence even began tracking how many times companies said “AI” on earnings calls, publishing a leaderboard of buzzword frequency. The message was simple: mention it or risk a markdown.

But saying AI is not the same as doing it, and doing it is not the same as making it work.

The Pressure Cycle

Behind every shiny “AI initiative” sits a familiar motive: rates are high, growth is slow, and executives need something that sounds like progress.

A 2025 MIT Media Lab / Project NANDA study found that 95 percent of corporate AI deployments never progress beyond pilot testing.

It is the enterprise version of downloading a new productivity app, trying it twice, then returning to email. That is the real state of “AI transformation.

Yet the vocabulary keeps expanding.

According to FactSet’s transcript analyzer, mentions of “AI” in S&P 500 earnings calls jumped 140 percent year over year, even as R&D spending declined 7 percent (source: OECD Economic Outlook 2025).

When Apple’s Q1 2025 call underplayed AI, its stock fell 2 percent in after-hours trading. Within a quarter, CFOs across sectors became part-time copywriters. PwC’s Global CEO Survey 2025 found that 78 percent of executives feared being perceived as lagging on AI more than actually falling behind on capability.

When language becomes currency, everyone starts minting words.

Executives are not lying; they are hedging uncertainty with narrative.

It is the same playbook seen during the dot-com boom and the early electrification era, when mentioning a technology signaled modernity regardless of function.

Finale: Why It Matters

The world is noisy right now — AI headlines, Fed minutes, our parents, layoffs, “efficiency” campaigns.

But underneath the noise, there’s a rhythm.

The Indie Investor reads that rhythm instead of reacting to it.

This field guide distills the signals that matter — the policies, prices, and behaviors that shape where capital flows next.

Read Policy, Not Headlines

Every Fed meeting is a map of money’s mood.

When rates rise, risk compresses. When they fall, courage expands.

Don’t wait for media translation. Read the Fed’s minutes yourself.

If policymakers say “restricting demand,” assume slower innovation.

If they say “sustained growth,” prepare for liquidity returning.

Policy is prose with investment subtext. Learn to read it fluently.

Move: Align your risk to the cycle.

High rates → accumulate durable assets.

Declining rates → rotate into growth and innovation.

Timing beats prediction.

Follow the Cost of Capital

The invisible hand moves through yield curves, not headlines.

When the 10-year Treasury yield climbs, expansion slows.

When it drops, venture wakes up.

Track 10-year Treasury yield, Fed Funds Rate, and M2 money supply.

These are your real sentiment indicators — the heartbeat of markets.

Move: Treat capital costs like weather.

You don’t control them, but you can sail with the wind.

Buy Fear, Sell Fashion

AI is the market’s current costume — beautiful, loud, and mostly theatrical.

Executives say “AI” to sound modern, not necessarily to make money.

When hype rises faster than revenue, opportunity hides in the shadow.

Move:

Invest where story exceeds substance.

Look beneath the headline themes to the enablers — the data layers, workflow tools, and compliance systems that actually power adoption.

That’s where compounding begins quietly.

Watch the Lag

Markets and people move on delay.

Rates rise months before layoffs hit. Optimism returns before the first earnings beat.

The space between signal and reaction is where alpha lives.

Move:

Track your own sentiment lag.

Note when you feel bullish or fearful versus when the market actually turns.

Over time, you’ll learn your emotional timing — your personal cost of capital.

Build While They Pause

When liquidity tightens, big firms freeze.

That’s when the independent class gains ground — the builders, freelancers, and retail investors who don’t need board approval to move.

This is your moment to compose, not conform.

Build something that outlasts the cycle: a small brand, a product, a syndicate, a portfolio of conviction.

Because when rates fall again, the market will reward what was built in silence.

Keep Your Own Score

Ignore quarterly noise. Measure your progress by participation, not prediction.

How many assets do you own that earn while you sleep?

How many projects did you fund before they trended?

How often did you act before consensus formed?

That’s your alpha.